The Economy

Two major investment themes, Brexit and U.S. – China trade war, showed progress last week. Both issues have been an impediment to capital investment and global growth. We have always maintained that resolving these would serve as a catalyst for global growth.

Boris Johnson won a landslide victory and helped bring a majority to his Conservative Party with his slogan, “Get Brexit Done.” Johnson has pledged to resolve Britain’s separation with the European Union by January 2020.

Chinese and U.S. leadership have announced that a Phase One trade deal has been agreed to by both parties. According to our analysis, the Chinese agreed to buy at least $40 billion of U.S. agriculture products, and the U.S. has agreed to roll back tariffs on certain Chinese goods. It is not clear when work on a Phase Two deal begins; however, the U.S. has indicated that they would begin in January.

In addition, the White House announced a rewrite of the North American Free Trade Agreement (NAFTA) last week. NAFTA was the cornerstone trade agreement put in place in 1994 between the U.S., Mexico and Canada. The new U.S. – Mexico – Canada Agreement (USMCA) incentivizes higher wages, domestic manufacturing and allows for independent unions. The deal prohibits tariffs on many products, including electronics, protections for intellectual property, and requires anti-spam laws. Bottom line is that the resolution of both these issues will help stimulate global growth and serve as a catalyst for stock prices over the near term.

Global Monetary Policy

Not surprisingly, the Fed left short term interest rates unchanged this past week at their December meeting. Over the past year, the Fed lowered rates three times, each time 25 basis points. We expect that the Fed will leave rates alone during the first half of the year as the economy responds to stimulus that is already in the system. With current stimulus combined with the potential resolution of Brexit and U.S. – China Trade war, the next move from the Fed may be to raise short term rates if economic activity accelerates.

The problems in the overnight repo market continue to persist. Since September, the Federal Reserve has stepped in repeatedly to support the repo market. A study released by the Bank for International Settlements (BIS) last week points to a shortage of lendable securities and the concentration in the repo lending market to just four banks. This is a structural problem in the capital markets following the Financial Crisis in which banks are less incentivized to lend in the repo market given current capital level policies.

Christine Lagarde, the new president of the European Central Bank, held her first news conference last week following a meeting of the bank’s Governing Council, which made no changes to monetary policy. Lagarde has promised to be different than other central bank leaders. We expect that she will lead an analysis of European monetary policy effect on climate change and income inequality, and other social issues that impact European Union citizens. Lagarde faces a significant challenge in dealing with indebted countries like Italy and trying to normalize monetary policy. We expect the ECB quantitative easing program will remain intact next year.

Equities

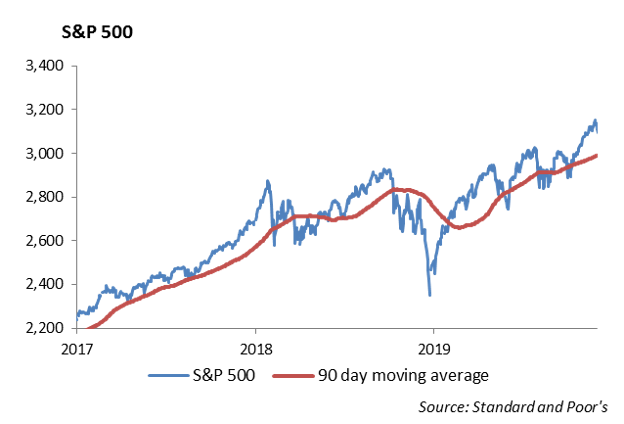

Stocks rallied this week on reports of a partial trade deal with China. Year to date gains are 20.6% for the DOW, 31.6% for the NASDAQ, and 26.4% for the S&P.

Gains continue to be broad based in each sector. Looking at 200 day moving averages: Financials, Health Care, Industrials, and Technology all have over 80% of stocks in the S&P trading above their moving averages. Energy and Real Estate are the only 2 sectors that are below 50%, although both are still positive for the year.

Costco reported earnings of $1.73 that beat by 1 cent. Revenue was $37.04 billion which was up 5.6% YoY and missed by $300 million. Comparable sales were up 5%, which was in line with expectations, and shares were unchanged on the earnings release. Costco is a name we continue to like, but it is at a slight premium in terms of valuation. Our thesis centers around their strong membership model, with a 90% renewal rate. They are constantly adding value to their membership services, and even with a price hike in fees, membership continues to increase both in the U.S. and worldwide. Costco is up 43.28% YTD, while the consumer staples sector is up 23.6% YTD, which we continue to be neutral on.

Oracle shares were down 3% on their earnings release with a revenue miss. Earnings beat by 2 cents, but both their Cloud Service & License Support segment and Cloud License segment missed expectations. They have had a bumpy ride since the passing of their CEO this year, but the stock is still up 21% YTD. The S&P Tech Sector is more than doubling those returns. At 14x earnings, and 12x cash flow, its currently trading at a 30% to the tech sector. Although we prefer a name such as MSFT, we still see ORCL as a solid holding. Earnings for the week include FedEx, Micron, Accenture, Conagra, and Nike.

Fixed Income

Interest rates continued to experience a rollercoaster ride of volatility on the wake of a Fed meeting, ECB press conference, and an increased likelihood of a phase one trade deal. The 10-year was wider by 10bps on Thursday after tweets from President Trump announced a victory in negotiations with China. The rate rally quickly faded on Friday as rates dropped 9bps to end the week little changed.

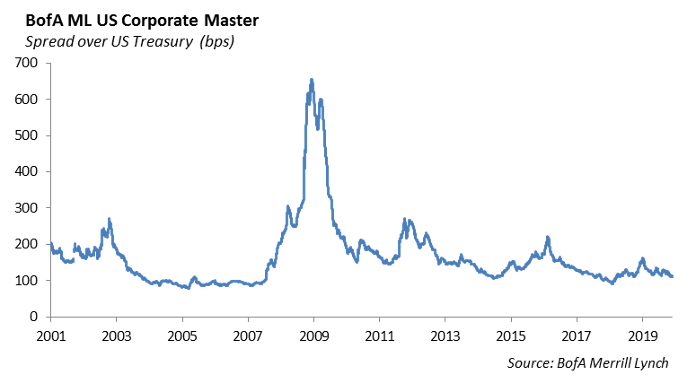

Credit spreads continued to tighten during the week, and the index is now below 100bps in spread. While we are not at all time tights, we certainly are at historic tights. A general lack of new issuance and low volatility across markets has favored spreads in the fourth quarter. We are cautious at current levels, and while we remain invested in spread product within five years, we have largely removed spread duration out the curve. At current levels, it is not a question of if, but rather, when the market will dislocate.

High Yield

The high yield index tightened almost 20 bps last week on trade optimism. High yield spreads are now at their lowest level since April. The week saw notable outperformance in the CCC tranche, which was the total return “winner” by more than a percentage. High yield fund flows were positive by just short of a billion dollars.

New issuance was quiet, with CenturyLink’s issuance pricing at the beginning of the week the lone notable issuance. Eldorado Resorts and US Steel remain on the calendar, but at this point, it would be a surprise if they came before the new year.

Going into the end of the new year, here are some of the characteristics we are looking for in potential high yield buys and some names that fit the criteria:

- Focus on the Balance Sheet: With spreads at lows since April, we want to remain defensive in our high yield allocation. Issuers who have stated that they will keep free cash flow focus on debt reduction rather than share buybacks and increased dividends will provide better defense in a spread widening environment. An example of this is CenturyLink 5.8% 3/15/2022, which cut 50% of its dividend earlier in the year to reduce leverage, but carries a single B rating which leads to the next point.

- High(er) Quality: Fitting in with the last point, in a compressed spread environment, high yield names with BB or BBB ratings allow portfolios to play defense. Issuers that are committed to retaining their high BB ratings or have investment grade aspirations should hold up well if spreads end up gapping out. An example here would be Centene 4.75% 5/15/2022, which holds a Ba1 and BBB- rating.

- First Lien: Issues backed by collateral offer piece of mind in case of a downturn. A first lien on collateral shows the investor how they would be paid if the worst were to happen. It also enhances credit quality. An example here would be Tenet Healthcare 4.625% 7/15/24 and ADT 6.25% 10/15/21.

- Positive Spread: In a low interest rate environment like today’s, high yield issuers have plenty of incentives to refinance their debt. Because of this, investors should be wary of buying anything with a negative spread. High coupon issuances with companies that still have access to the capital markets have plenty of opportunity to refinance and make investors realize the negative spread they bought at. An example of an issuance we have ruled out due to negative spread and yield is Iron Mountain 6% 8/15/2023, even though it checks a lot of our boxes on credit quality and a high yield to maturity.

Please reach out if there is interest in any of the names listed here or if you would like to see how a different name fits into these criteria.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.