Before this year’s end, we expect the Federal Reserve will begin to shift away from the aggressive monetary policy that has provided support to the capital markets since the start of the pandemic in March last year.

With the increase in vaccinations and more of the economy reopening, we expect GDP growth to accelerate over 6.25% this year. We expect economic activity to be strong in the second half of the year. The increase in economic activity will put pressure on the labor market as service businesses, including travel and entertainment industries, increase staffing as demand surges.

The increase in economic growth and expected inflation will be enough to push the Federal Reserve to move short term interest rates higher. Typically, a shift in monetary policy toward higher rates will suppress returns in risk assets, and we expect the domestic equity market will experience increased volatility at the first sign of a change in monetary policy direction. If history is a guide, this shift in monetary policy will be slow and intentional in order to minimize market disruptions.

Former Treasury Secretary, Larry Summers, is leading a criticism that the Fed is providing too much stimulus to an economy already rebounding from the pandemic, which could potentially endanger its long term fiscal health. These sentiments will provide cover for the Fed to justify the policy shift.

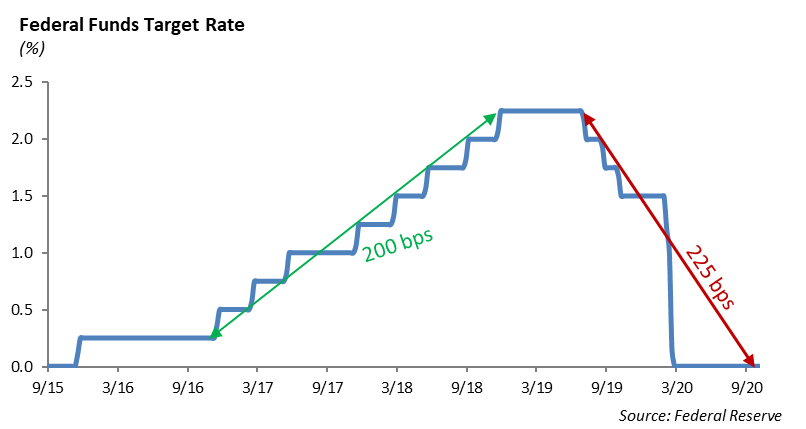

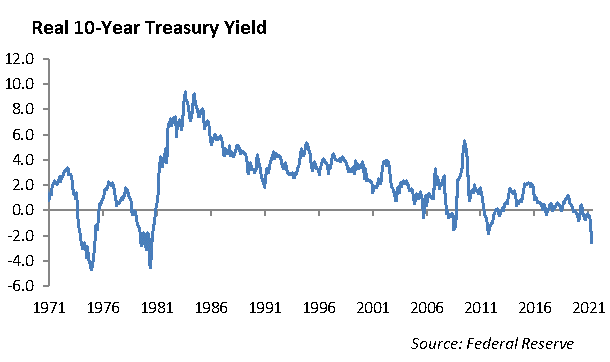

The Fed’s playbook to shift policy will look similar to the withdrawal of stimulus in 2017 following the Financial Crisis. The Fed took tentative steps to increase the Fed Funds rate over a two-year period in 25 bps increments from 2016 to 2018. During this same period, the Yield on the 10-year US Treasury increased from 1.5% to 3.2%. This increase in yield was in a benign inflationary environment in which expectations for inflation were more subdued than today. The increase expected rate of inflation will pressure real yields on US Treasuries, the difference between the nominal yield and expect inflation, into negative territory compared to 2016 – 2018.

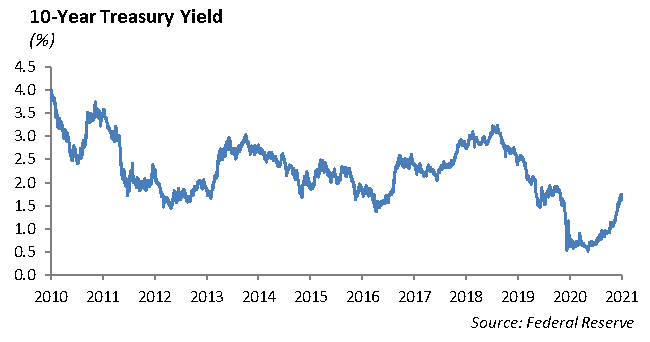

With the yield on the 10-year US Treasury trading at roughly 1.65% today, the markets are not discounting the inevitable Fed tightening coming later this year. Layer on the current trend toward rising inflation, and we would argue that yields should shift higher.

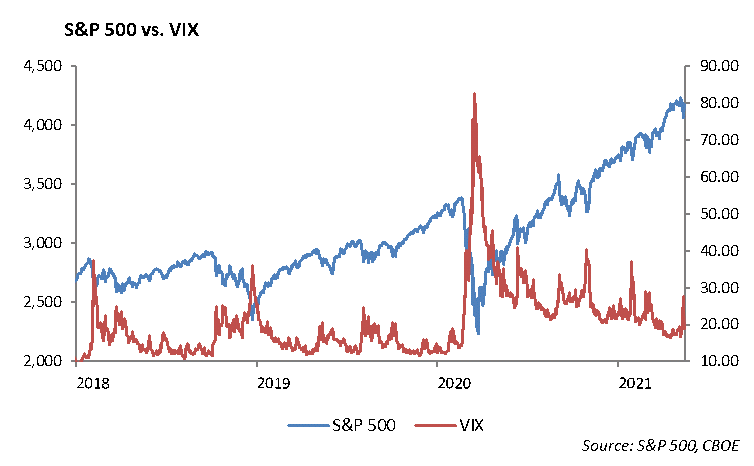

The S&P 500 struggled over the two year period moving from roughly 2200 to 2925 before falling to 2400. Given current valuations of S&P 500 at a 37.1 P/E Ratio, we expect significantly lower returns in domestic equities over the next several years if the Fed attempts to normalize monetary policy.

Equity

While the S&P 500 traded down -0.43% last week, finishing -3% off of all-time highs, it is still up over 10% year to date. The rotation out of technology stocks continues to weigh on the overall market. Even though the Nasdaq index rose 2% on Thursday, the index is up 4.5% year to date, lagging the S&P 500. The technology sector continues to lag the market with a meager 4% return this year, making it the worst performing sector next to Consumer Discretionary. Energy and Financials lead the way, returning 36% and 27%, respectively.

Earnings season is winding down, with over 90% of companies in the S&P reporting earnings. Over 85% of companies have reported revenue above expectations. Last week, Home Depot and Lowe’s provided further insight into the home improvement space.

Home Depot [HD]

Home Depot reported earnings of $3.86 per shares, ahead of consensus of $3.08 per share. Revenues of $37.5 billion was ahead of consensus by $2.5 billion and up 31% year-over-year. U.S. Comps were up 30%, ahead of 24% expected. All commodity prices were a positive impact of 375 basis points on comps. Lumber prices negatively impacted gross margins by 35 basis points, and gross margins were down -10 basis points overall. The company did not provide guidance for 2022, sending the stock down about -1% on its earnings release.

Lowe’s [LOW]

Lowe’s reported earnings of $3.21 per share, ahead of consensus of $2.61 per share. Revenues of $24.4 billion was up 24% and ahead of the $23.8 billion consensus. Comps were up 26%, also ahead of the 21% expected. The company is up about 18% this year, the same performance as Home Depot. Both companies have benefited from the current real estate market and have outperformed the broader sector. Both companies will face tough comps going into next quarter, as these stores remained open during lockdown. Additionally, with states opening up and individuals dedicating their time to other things, it will be difficult for this segment to continue to outperform as the home improvement projects may stall. But at 18x earnings and 12x free cash flow, Lowe’s is still the cheaper pick compared to Home Depot within the space.

Fixed Income

Bond yields continue to trend higher consistent with the economic recovery and rising inflation narrative that has caused volatility in the stock market. The recent sharp declines in the prices of equities, gold and Bitcoin are good reminders of the importance of a thoughtful asset allocation.

While bond yields remain historically low, credit spreads tight, and expected returns muted fixed income continues to be one of the best strategies to diversify asset allocation given sustained low correlations to broad equity indexes. In 2021, the S&P 500 has had a 0.15 correlation to the U.S. Aggregate Index and a -0.51 correlation to 30-year U.S. Treasuries.

New issue investment grade corporate market remains active with $753 billion issued through April. Overall, new issuance is down -16.1% year-over-year which is not surprising given the sustained low level of interest rates. The Fed has effectively orchestrated an interest rate environment that has provided a subsidy for corporate America to refinance their debt and term out their maturity structure.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management