The Economy

Our base case for the economy remains that the vaccine will be effective in controlling the spread of COVID-19, which will clear a path for the economy to reopen and economic growth to rebound. The increase in demand will put pressure on inflation and wages as we expect a labor shortage in the second half of the year.

We expect GDP growth in 2021 to exceed 6.25%.

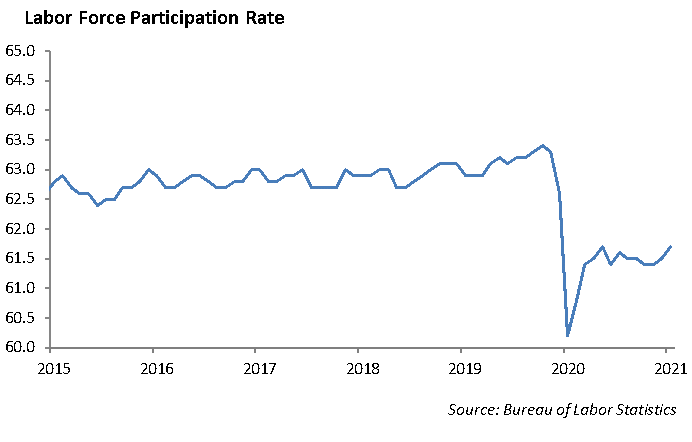

Over 8 million people are still out of work. However, the labor shortage we expected in the second half of the year has already hit the markets. The reopening of restaurants and entertainment venues has put pressure on the labor pool that was largely dislocated last year during the pandemic. While there is marginal improvement in the labor force participation rate, the increased demand for labor is compounded by the extended unemployment benefits, providing a comfort cushion for workers choosing to stay home.

Disruptions in supply chains, shortages of certain foods and commodities, and an increase in construction have combined to put pressure on prices for many goods and services. This price pressure is compounded by a series of trade tariffs in Europe and China.

We expect the consumer to lead the recovery in the second half of the year. Retail sales surged by 10.7% in March and remained flat in April, according to data from the Census Bureau. The slowdown in April reflects the somewhat fickle nature of the services sector. However, we believe this doesn’t completely reflect the increased consumer spending that is creeping through the economy. We expect the relaxed mask mandate, increased savings, a strong labor market and rising wages will all fuel the consumer sector to higher spending. In addition, with travel, entertainment and professional sports opening up, there are more opportunities to spend money.

Inflation – Not Translating Into Higher Interest Rates

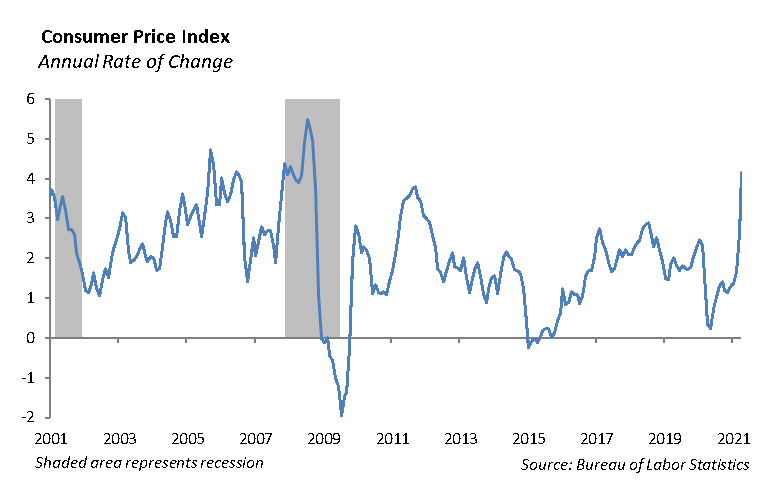

The Consumer Price Index for All Urban Consumers rose 0.8% on a seasonally adjusted (SA) basis in April and 4.2% during the last 12 months, not seasonally adjusted (NSA). When food and energy is removed, the CPI increased 0.9% in April (SA) and 3.0% during the year (NSA).

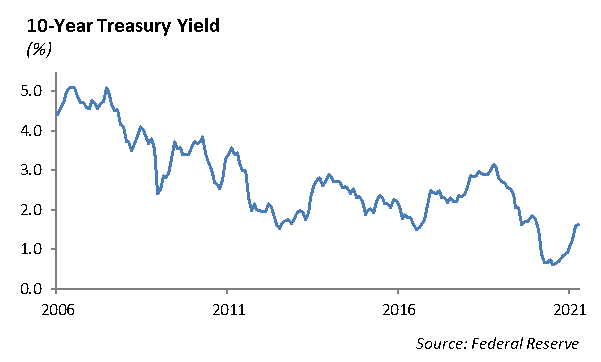

The increase in the rate of inflation has not translated into an increase in U.S. Treasury yields. After hitting a high of 1.75% at the end of March, the yield on the 10-year U.S. Treasury has fallen to 1.63%.

Much like a wounded ship inching its way back to port after a storm, the domestic economy is trying to survive the shutdown caused by the pandemic. The Fed has been looking for this scenario of higher inflation and accelerating economic growth. It has been doing its part to talk yields lower while allowing the rate of inflation to move higher. This is not unexpected.

The domestic economy has significant excess resources available, including labor and manufacturing, which will need to be absorbed for sustained inflation to push rates higher. We expect marginal improvements in the supply-chain disruptions and with the expiration of the extended unemployment benefits this summer will combine to absorb some of the slack resources, pushing interest rates higher.

Higher Rates and the Impact on Asset Valuations

Higher interest rates are causing disruptions to asset valuations, particularly domestic stocks. The S&P 500 is up 11.1% year to date and 46.3% on a trailing 12-month basis. The performance is impressive given that roughly $600 billion of the economy is still not open. However, the increase in US Treasury yields has resulted in heightened volatility and a sell-off in the Technology sector.

The yield curve has steepened significantly with the 2-10 Year spread pushing out to +145 bps. The steepening yield curve is expected given the outlook for strong economic growth. The broader recovery stocks have performed better than Technology on a relative basis. Energy and Financials have posted some of the strongest performance so far this year, up 40% and 28% respectively.

We expect the improved economic recovery will result in higher interest rates and increased volatility. While the journey through higher rates will prove disruptive to equity markets, it does not mean selling stocks and moving to cash. We experienced a similar scenario in 2013 when interest rates moved higher, and the S&P 500 was up 32.4% for the year. At the end of the day, looking past fundamentals, the extraordinary monetary and fiscal stimulus provide a significant incentive for investors to remain invested in domestic equities.

Still, problems remain in the economy. The pandemic continues to impact commercial real estate as office vacancy rates remain high across the country. The shifting higher education business model of remote learning, high tuition and high fixed costs remains unaddressed. The growing student loan debt burden weighs on college graduates. And the underfunded public pension plans remain in place as the aging demographics of our population shift higher.

Equity

Markets traded off of all-time highs last week with the S&P giving back 1.4% during the last five days. On Wednesday, the index fell more than -2% on concerns of rising inflation. The Technology and Consumer Discretionary sectors were hurt the worst, as both segments fell more than -3%. Year to date, Technology is now the biggest laggard. This high growth sector is currently returning 4%, the worst of any sector. The pullback can also be seen in the Nasdaq, as the index is trading more than -6% off of all-time highs. Investors continue to favor value sectors, with Energy and Financials continuing to outperform the broader market. The Energy sector is up more than 40% this year, and the Financials sector is up 28%.

More than 80% of companies in the S&P have reported 1Q earnings. Of those, 77% have beaten sales expectations and 85% have beaten earnings expectations. Consumer Discretionary is the sector to watch this week, as a number of companies are on deck to report, including Home Depot, Lowe’s, Target, TJX, and VF Corp.

Walt Disney Co [DIS]

Disney reported earnings that beat expectations, but its revenue missed consensus by $320 million. Revenue was $15.61 billion, which fell -13% year-over-year. Disney+ subscribers were 104 million, which also missed the 109 million consensus. The stock is lower by -3%, given its revenue fell worse than expected, and streaming didn’t mitigate the losses from their parks segment. The two bright spots are their other streaming services. ESPN Plus was up 75% year-over-year, and Hulu subscribers were 42 million, up 30%. Average revenue per user rose 7% at ESPN and 21% at Hulu. The company did reiterate their forecast for 2024 of 230-260 million subscribers. We believe that the stock is currently overvalued given the struggles it has had in its parks segment. Free-cash-flow generation is unlikely to recover in full until 2022 at the earliest, with just $3 billion for 2021. As a result, multiples are at very high levels relative to historical averages, and with the stock still trading near highs, it is difficult to see near- term upside. However, the long-term forecast still looks great, led by rapid streaming growth and EPS recovery through the reopening of its parks segment.

Fixed Income

Interest rates have remained stubbornly range bound during the past several trading sessions, despite a much larger than expected inflation number. The rate on the 10-year U.S. Treasury remains near 1.65%. The global economy is undoubtingly showing signs of recovery; however, with global negative yielding debt still at $13 trillion, and rates unchanged, the bond market is projecting a different outcome for growth and inflation.

High yield credit continues to be the unstoppable force in fixed income markets. While long-end U.S. Treasuries have had a total return of -12.64%, the Bloomberg Barclays High Yield Index is up 1.30% year to date. As pension funds and some insurance companies reach for yield, inflows into high yield have increased and spreads have tightened 50 bps in 2021. With both spreads and yields at five-year lows, investors do not look adequately compensated for their risk. While we still think corporate credit outperforms in a low volatility environment, we currently prefer an up in quality tilt given asymmetric risks in the market. We see an upgrade potential to AAA status in companies such as Apple, Google, and Amazon, which have more cash than debt and are running cash-flow machines. Conversely, if the market dislocates, these credits will experience much less volatility than low BBB or high yield credits, giving us the ability to shift the portfolio into better values at that time.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management