“Government policy is created and carried out through force, and that force creates unintended consequences that do not come from voluntary trade.” – Milton Freidman

In an effort to combat rising inflation, the Federal Reserve’s relentless push to increase short term interest rates is designed to shift the demand curve and make it harder for consumers to buy cars, houses and other things. And, it is designed to incentivize business to reduce labor expenses by laying off part of the work force. All of these will help to slow economic growth. However, it is not designed to put Silicon Valley Bank out of business; but, that was the unintended consequence.

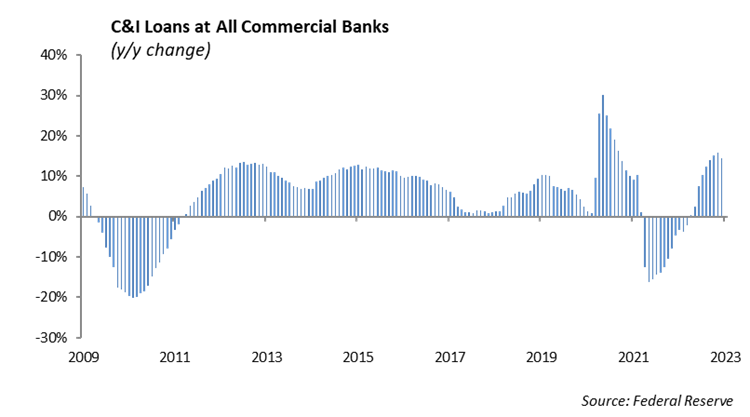

Following the Financial Crisis in 2008, banks sat on a large deposit base in the face of shrinking loan demand. Total loan and leases for commercial banks eventually increased from $6.486 trillion in April 2011 to $10.827 trillion in May of 2020. However, the pandemic resulted in excess deposits at banks and a sharp decline in loan demand. Depositors earned very little during the pandemic; however, with the sharp increase in short term rates, many banks lagged paying higher interest rates on their deposits. After all, banks could afford to lose the excess deposits on the balance sheet.

But, during the pandemic, in the face of low interest rates and a sharp decline in loan demand, treasurers shifted the investment portfolio to longer US Treasury securities in order to pick up slightly higher yields. US Treasury securities are particularly capital efficient for banks at a lower risk-weighted asset charge.

In 2022, the Fed moved aggressively to push interest rates higher. The unintended consequence of this poorly executed strategy resulted in the ten-year yield increasing from .51% in August 2020 to 4.24% in October 2022. If every 10 basis points is roughly 0.80 in price on the 10-year bond, then 370 basis point increase in yield is 29.6 points on the price of a ten-year US Treasury bond. The change in interest rates translates to a loss of $5.22 billion on an $18 billion US Treasury portfolio.

With the rise in interest rates over the past two years and the associated tightening monetary environment, cash-burn from startups without access to additional venture capital saw their deposits balance dwindle. In order to generate liquidity to offset the deposit runoff, SVB needed to liquidate their more-liquid US Treasury portfolio at continually higher losses. The result was an erosion in their capital base caused by the losses in selling the US Treasuries, ironically considered safe, capital-efficient investments.

While SVB’s failure has caused ripples across the bank sector, it is important to note the liquidity crunch arose from poor asset-liability management rather than a systemic issue. The bank failures in the Great Financial Crisis arose from a worldwide credit issue on weak bank balance sheets. Banks across the board have stronger balance sheets, lower financial leverage and better regulatory oversight when compared to their counterparts in 2008. These factors, in conjunction with the Federal Reserve’s announcement of a new liquidity facility for banks in liquidity crises, may help prevent another widespread bank panic.

With competing priorities for the Fed, the first priority is to protect the financial system, which puts the fight against inflation to the back seat for now. We do not expect the collapse of SVB to result in a systemic problem for the capital markets or the economy. However, the recent decline in short term interest rates will provide a challenge for the Fed’s inflation fighting efforts over the near term.

Milton Friedman said, “One of the great mistakes is to judge policies and programs by their intentions rather than their results.” This Federal Reserve does not want to be known as the group that let inflation accelerate in the decade of 2020. While the intention is to reduce the pace of inflation, we suspect the results of the Fed’s initiative, when the dust settles, will have a significant impact on the economy and capital markets.

This report is published solely for informational purposes and is not to be construed as specific tax, legal, or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2023 Winthrop Capital Management