Economy

The U.S. economy showed signs of stabilization in the first part of 2021. Congress and the Fed are fueling the economy for a roaring comeback from the market downturn, and manufacturing is at its highest level since 2018. Widespread vaccine distribution is a promising sign for the reopening of several parts of the economy. However, more than 9 million people still remain unemployed, and we do not expect the economic recovery to be in a straight line. The second quarter is underway, and the following themes are emerging:

- Economic growth is already beginning to accelerate this year. Retail sales increased 9.8% in March versus a -3% drop in February, as stimulus checks and warmer weather prompted consumers to spend. We expect the gradual return to normal activity and the easing of business restrictions will support continued strong growth in the consumer sector.

- Job gains last month, the strongest since August of 2020, have also supported the economic growth narrative. The Labor Department reported first-time unemployment claims dropped to 576,000 last week, the lowest level since the beginning of the pandemic.

- The housing sector is strong with home prices rising across the country. Freddie Mac released a study last week that estimates there is a 3.8 million shortage of homes for first time buyers.

- Airlines report improved operations. American Airlines expects to be at 90% of 2019 capacity levels this summer, and Delta says it has recovered 85% of its domestic leisure ticket sales.

- The focus for the capital markets is on the potential for additional fiscal stimulus through an infrastructure bill as well as the continued reopening of the economy. At the same time, the runup in stock valuations is vulnerable, if not supported by improvement in operations to support growth expectations.

Equity

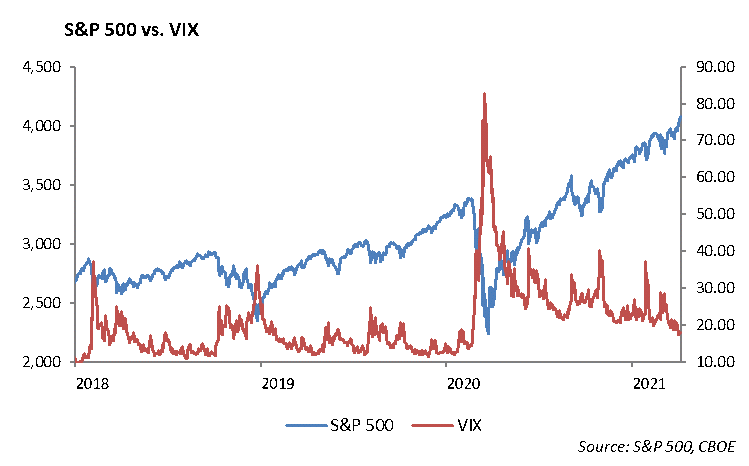

Earnings season has started for 2021 and it is looking like the year will deliver a strong rebound across many of the industries, including those heavily impacted by the pandemic. This quarter should provide a very similar result to the previous three that have set a historically elevated trend in beat rates. The season started with Financials crushing their estimates. The steepening yield curve, rally in stock prices, and expectations for a strong economic recovery support continued strength in financial stocks. Stock prices are soaring with S&P 500 increasing 11% and hitting new records this past year at 4185 and volatility falling.

Citigroup [C]

Citigroup reported profit of $7.9 billion, or $3.62 per share. This beat the $2.60 consensus estimate. Revenue of $19.3 billion also beat the estimate by $500 million. This was on a strong beat in investment banking revenues. Citi earnings benefited from a substantial reserve release. Of interest is that Citi, under new leadership of CEO Jane Fraser, announced they will be exiting consumer operations in 13 markets including China, Taiwan and South Korea. Citigroup wants to focus its non-US consumer banking on areas with a great concentration of wealth including Hong Kong, UAE, London, and Singapore. Shares were up 3% on its earnings release and up 18% year to date.

Morgan Stanley [MS]

Morgan Stanley reported a loss of $911 million as a result of its exposure to Archegos Capital Management and its implosion from leveraged, concentrated bets particularly in media companies. Adjusted for the Archegos loss, MS reported a quarterly profit of $4.1 billion, or $2.19 a share on revenue of $15.7 billion. The newly acquired E*Trade business showed strength given the increase in retail trading, with the Wealth Management division reporting more than $6 billion in revenue, an increase of 47% over prior period.

Blackrock [BLK]

Blackrock reported a first-quarter profit of $1.2 billion or $7.77 a share. Revenue grew 19% to $4.4 billion. Assets under management grew to $9 trillion. The company benefits from asset inflows across all its strategies – both passively and actively managed.

JPMorgan [JPM]

JPM posted first-quarter earnings of $4.50 per share, higher than the $3.10 expected. Revenue was $33.12 Billion, which also beat the $30.52 Billion estimate. This was mostly driven through their trading division. Fixed income trading revenue was $5.8 Billion, a 15% increase and a beat by $800 million. Equities trading was up 47% to $3.3 Billion, which was $1 billion higher than estimates. Investment banking revenue of $2.9 Billion was up from $2 billion last year. Asset & Wealth Management was up 5% quarter over quarter and 20% year over year to $4.08 billion. JPM shares are up 21% this year and were flat on the earnings release.

Goldman Sachs [GS]

Goldman Sachs posted earnings of $18.60, beating the $10.22 estimate. Revenue was $17.7 billion which beat estimates by $5 billion. Fixed Income trading revenue was $3.89 billion, Equity revenue was $3.69 billion and Investment Banking was $3.77 billion. Equities were up 68% and fixed income was up 31%. Investment Banking was up 73% from last year and exceeded estimates by $1 billion. This is due to a record in equity underwriting, which was significantly higher with strong initial public offerings. Asset management also generated record revenues of $4.61 billion. Shares rose 1% on the earnings release and are up 24% this year.

Bank of America [BAC]

Bank of America reported first-quarter earnings of 86 cents a share, beating the estimate of 66 cents a share. The company reported $22.9 billion in revenue, also beating estimates. Similar to JPM and GS, the bank saw a big boost in its trading operations. Fixed Income trading revenue was up 22% to $3.3 billion, and Equities rose 10% to $1.8 billion. Investment Banking fees were up 62%, due to a 218% increase in equity underwriting. Shares are up 32% year to date, one of the best performers among the big banks.

Kimco Realty [KIM]

Kimco Realty agreed to acquire Weingarten Realty Investors for $3.9 billion in cash and stock last week, which values Weingarten at $30.32 per share and an 11% premium over its market price. The combined company will have a market cap near $12 billion and a focused portfolio in the Sunbelt consisting of grocery-anchored shopping centers and mixed-use buildings.

Fixed Income

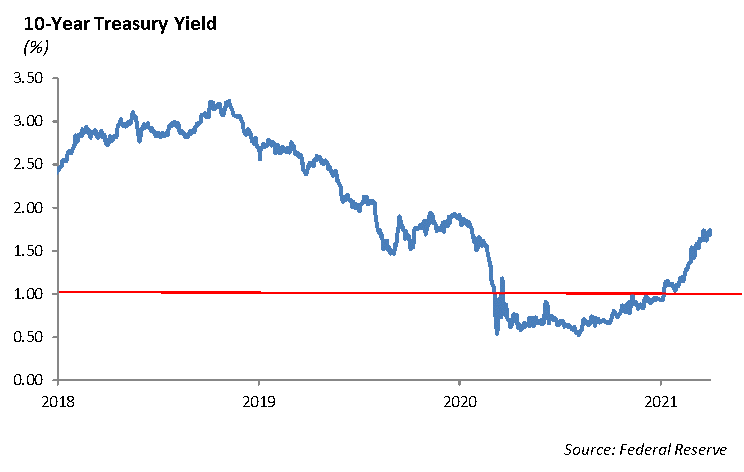

Strong retail sales and a lofty Consumer Price Index for March was curiously met with lower bond yields. The 10-year treasury was down more than 10 bps for the week, ending at 1.58%. Bond investors seem to believe that simply hitting short-term inflation expectations is not enough to drive long-term inflation. Treasuries rallied at the same time that equity markets continued to rise. This move could likely accelerate as short interest in long-term treasury ETFs are at all-time highs. While the U.S. economy continues to re-open and accelerate, it is too soon to say that inflation is not on the way.

The corporate credit story was dominated over the past week by primary issuance from the largest U.S. banks post-earnings. Both JP Morgan and Bank of America brought record-breaking deals at $13 billion and $15 billion respectively. This large amount of issuance is driven by strong earnings results and borrowing costs that are still at historically low levels. Issuance came with little to no concession, leading to underperformance in the secondary markets.

The heavy issuance and lower interest rates led to widening of overall credit spreads. Despite the widening, the spread on the investment-grade corporate index is at 94 bps, a historic low by any measure. We still prefer a more diversified, up in quality portfolio across our fixed-income allocations. This will allow us to continue to participate in a rallying market, while reducing downside risk in an overvalued market.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management