Economy

The International Monetary Fund (IMF) expects the world economy to expand by 6% this year, the fastest pace of growth since 1980. The new projection is an increase from the prior projection of 5.5% that the IMF made at the start of the year, and the optimistic outlooks is lead largely by the surge in economic growth by the United States and China.

Global output declined last year by -3.3% in the aggregate due to the pandemic, and the recovery has been choppy. After providing strong stimulus to its economy, China has shown an initial surge in growth and is expected to grow by 8.4% this year. The United States has pushed unprecedented stimulus through to businesses and households and is expected to grow by 6.5% this year.

Biden is pushing for a $1.9 trillion fiscal stimulus package which would support economic growth, and at the same time, increase corporate taxes. The new corporate tax rate would include a minimum corporate tax rate that would be coordinated across the developed countries, while attempting to close loopholes that companies often use to lower their tax rate. The new plan will be more of a headwind for stock prices and investors than for the economy.

Europe has had an uneven rollout of vaccines and the region is now struggling through a third wave of Covid-19 cases. The recovery will be muted in parts of Europe, and we expect it to impact the tourist season this summer.

Jamie Dimon’s annual letter to shareholders came out last week, and it’s a big one – 66 pages long. His annual letter to shareholders has become a “must read” in the financial world. In his letter, he points out the banks are playing an increasingly smaller role in the financial system, which is a growing risk for investors.

Office vacancy rates are at 16.4% nationwide, a high level by any comparison. As companies wrestle with maintaining revenue and retaining talent, they are able to rationalize expenses under extreme uncertainty as a result of the pandemic. The result is a near term decline in the demand for office space. Keep in mind, the trend toward an open work space has only grown in the past five years, all in the name of boosting morale, increased collaboration and talent retention. We believe the reduction in office space is driven by companies’ desire to increase profits and has less to do with allowing flexibility of employees to work remotely. If you manage a company with workers operating remotely, you know firsthand the difficulties of accountability and collaboration. We expect the trend will be reversed as managers reassemble work teams into office space once the pandemic resides.

Monetary Policy

Federal Reserve Chairman Powell has made it clear over the past weeks that the Fed will do everything in its power to continue to provide stimulus to the market. He emphasized the economic growth is still not stabilized, and we are still at risk. While we disagree with the assessment, we understand the need to assure investors that the Fed is not pulling the plug yet, because of the potential negative impact on capital investment, labor, and stock prices.

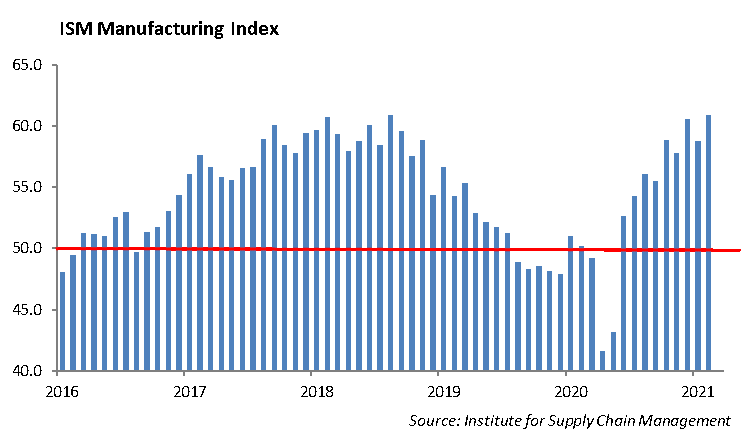

One of the bright spots highlighted by Chairman Powell in the economic recovery has been the rebound in manufacturing with the ISM Manufacturing Index up over 60.

Equity

We are heading into 1Q 2021 earnings season, and we expect it to be strong. The equity market in the first quarter was defined by the rotation out of the high-tech stocks that performed well last year into the companies that were greatly impacted by the pandemic. While we could call it a simple rotation into cyclicals, or value stocks, that description doesn’t fully depict what is happening.

March was a tough month for Apple, Microsoft, Amazon and Alphabet, but all are up over 6% in April with a surge in big technology stocks. The stay-at-home stocks, such as Paypal, Etsy, ServiceNow and Autodesk have been hardest hit this year, but are having a strong resurgence in April. As long as the Federal Reserve is pouring money into the system, stocks should perform well. The choking point will be how rising interest rates impact valuations. Volatility has declined with the sharp rise in stock prices.

Fixed Income

Growth and inflation expectations have driven rates across the globe higher over the first quarter. The 10-year U.S. Treasury began the year at 0.913% and is currently the low of the year. The 10-year currently trades at 1.65%, after fading from a year-to-date peak of 1.74%. Global negative yielding debt also peaked at year end. After surpassing $18 trillion, negative yielding debt has fallen to $14 trillion. While we see a case for U.S. rates to rise, we believe global rates will continue to stay compressed as their growth outlook has substantial headwinds.

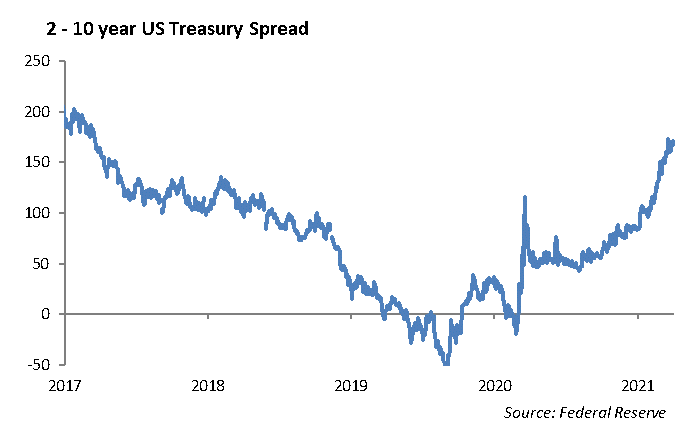

The slope of the yield curve underscores the significance of the economic recovery we are experiencing. The yield curve continues to steepen and we expect 2 – 10 year spread to hit 200 bps.

Corporate bonds began the year at historically tight spreads, and have continued to tighten as interest rates have risen. High yield spreads have tightened over 50bps as investors chase any yield they can find. The high yield index currently yields 4.06%, the lowest yield ever despite a rising interest rate environment. While economic growth and credit look generally strong, markets are beginning to look overvalued. We would continue to hold credit across fixed income portfolios but are moving up in quality on the long end of the curve. This is done with a combination of A-rated corporates and U.S. Treasuries.

With interest rates at historical lows, we see returns in fixed income markets compressed over the near term. We believe fixed income should still play a critical role in an asset allocation. It continues to be the most uncorrelated asset class to equities, and given the expanded valuations across stocks, bonds would provide risk mitigation in the event of a down turn. We prefer the up in quality trade, and would caution income investors from chasing yield by taking on increasing credit risk.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management