The Economy

Just as we turn the corner from a year dominated by the pandemic, with hopes that normality might return in 2021, the stomach-wrenching riots in the Capitol last week swept the news. Roll up your sleeves, this year is likely going to get messy, and we don’t mean that just in a political sense. As investment analysts and portfolio managers, we aim to keep politics out of our reports. However, there are few times when politics have a significant impact on valuations, market activity and volatility. The two-party system that operates within our democracy has forced a gridlock in the legislative branch for nearly 15 years. So far, indications point to Republicans in Congress making it a difficult first year for the Biden administration.

For the past decade, we have written about the evolution of our democracy and its impact on capitalism. In the world today, we effectively have two systems of capitalism, Western democracy of the United States and state-controlled capitalism preached by China. For investors, the next decade will be defined by the competition between these two countries and their respective form of capitalism. During the past decade, China has been executing its plan to further integrate into the world economy on its terms. In spite of the recent initiatives to de-list Chinese companies linked to their military, we expect China will make significant gains this decade in growing their global competitive position. One example, and a reason we are concerned about Tesla’s stock valuation, is the threat of a global Chinese car manufacturer taking market share in the electric car market.

The key driver to capital markets is the ability to effectively control the spread of the COVID-19 virus. The pandemic is the main cause of the global economic challenges, and the expectations are that it will end in 2021. We are at the intersection of the spreading coronavirus and the rush to distribute a vaccine.

At the end of last year, the government enacted legislation that will provide more than $900 billion in support for consumers and businesses. Fiscal stimulus, combined with the Federal Reserve’s aggressively accommodative monetary policy, will be the fuel that supports equity valuations. There is a reasonable chance that President-elect Biden will be able to deliver more aid to people in need with a now Democratic-controlled Senate. In addition, we expect Congress has to offer some assistance to state and local governments whose financial condition has deteriorated as a result of the coronavirus and the sharp decline in tax revenue.

Equity Market Valuation

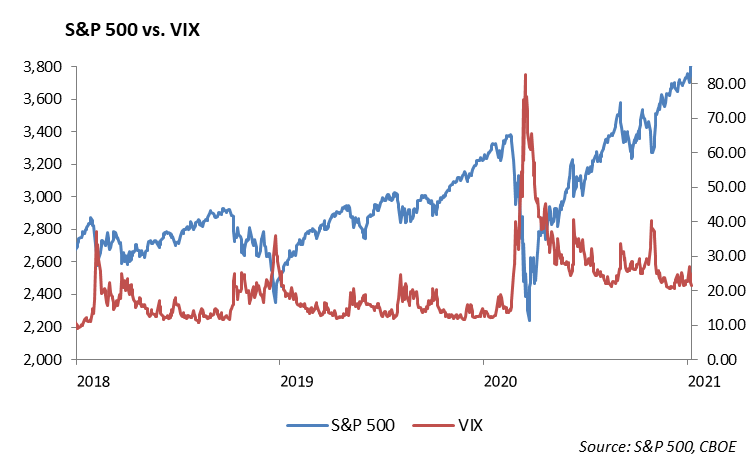

The equity markets have continued the rally into the New Year. The S&P 500 has gained 1.8% already year-to-date and is trading at all-time highs of 3824. The energy, materials, and financials sectors have each started the year off strong. With the rebound in oil prices, the energy sector is up 9% in 2021. The NASDAQ is also at record highs and is already up 2.4% this year. Volatility creeped higher last week, with the Capitol Hill riot causing large daily swings, specifically in the technology sector. Chinese stocks were most affected, as Trump has continued to target them for de-listing in the United States.

Chinese tech stocks have been increasingly volatile lately, with continued rumors of a U.S. ban. In November, the U.S. government blacklisted more than 30 Chinese companies that were supporting China’s military. After going back and forth on their decision, the New York Stock Exchange confirmed that it plans to delist telecommunications giants, China Mobile, China Telecom, and China Unicom. Further rumors that this delisting could affect both Tencent and Alibaba forced shares of both companies to trade down more than -4%. In spite of a recent anti-monopoly investigation into Alibaba, we believe the stock is a long-term buy. Alibaba is the clear leader in e-commerce, cloud, and mobile payments in China, and after weathering the trade war for years, its dominance will not disappear any time soon. What is even more surprising is the reaction to Tencent, a reasonably priced company that has proven to be adaptable to regulatory changes. Its major segment, gaming, will continue to experience remarkable growth in 2021, as China’s consumer spending on games will exceed the U.S. with a forecast of $44 billion in 2021. As the Chinese government specifically targeted Alibaba and Jack Ma, Tencent was punished, despite no direct impact to their business. We believe the selloff in both names offers an attractive entry. A good way to gain exposure to both names is the KraneShares CSI China Internet ETF [KWEB]. These stocks make up 18% of the ETF, and we have initiated positions in our models.

Shares of Twitter (TWTR) declined -6% on Friday, following the announcement that it has permanently suspended the account of President Donald Trump. The ban followed last Wednesday’s events, when Trump spoke to a rally of supporters, who later stormed the U.S. Capitol Building while Congress was voting to confirm the election results. The @POTUS account had more than 88 million followers. In addition, Twitter announced that the accounts of former national security adviser, Michael Flynn, and Trump lawyer, Sidney Powell, have also been permanently shut down. In 2020, shares of Twitter nearly doubled in value as the technology sector rallied.

In addition, Facebook, Apple, Snap, Reddit and Pinterest have announced that they have banned Trump from their platforms. This will likely elevate the debate on censorship and free speech under the first amendment.

Fixed Income

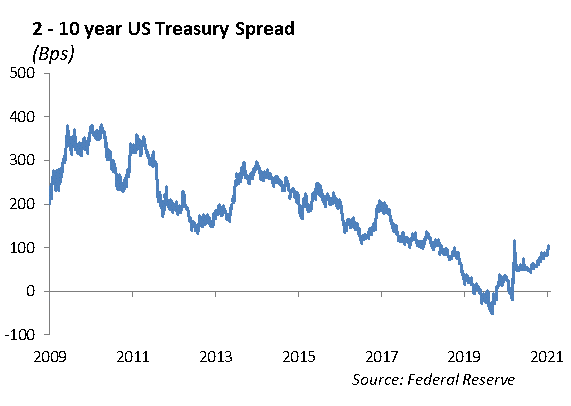

Heading into a new year, interest rates are at extraordinary low levels and have not yet normalized to pre-pandemic levels. However, with the expectation for an economic recovery later this year, we expect to see rates drift higher. The Federal Reserve has indicated that it intended to keep interest rates low for a sustained period of time, which will help support valuations in the stock market and other financial assets.

Last week was a volatile week for bonds. The yield on the 10-year U.S. Treasury traded above 1% for the first time since March of 2020 and ended the week at 1.11%. The Treasury curve also steepened roughly 20 bps, driven by the Democrats securing control over the Senate and opening the door to further and sustained fiscal spending out of Washington. Inflation fears re-entered the minds of investors, and 10-year breakeven yields rose 10 bps. We are not surprised by this move up in rates and ultimately believe rates will continue to stay range bound and move lower.

Corporate credit was met with a buying frenzy last week as interest rates rose and credit spreads tightened. It was difficult to buy bonds without being aggressive, as investors wanted to take advantage of substantially higher rates than what we’ve seen in almost a year. Credit spreads were pushed to their tightest level since 2014, leading to a slightly overvalued position in both investment grade and high yield bonds. We have continued to move up in quality as the amount of further tightening potential is far smaller than the spread widening potential. With that said, barring any unforeseen credit event in the market, we expect spreads to continue to tighten as new issuance throughout the first quarter is expected to be light. Regardless, we are tactically reducing the overall volatility of our portfolios over the near term.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management