Risks to the Market

We have quickly become accustomed to new vocabulary words, such as “double vaxxed” and “Covid variant.” The global pandemic continues to shape the capital markets, global economic growth and how investors view risk. A market is a clearinghouse for the price of risk. Markets have a way of digesting risks and adjusting price level and volatility as risks are adapted into market prices. One of the risks today is the spread of new Covid variant mutations. The new Omicron variant, which is emanating from South Africa, is the risk that now weighs on the markets. We are living in a world in which new Covid mutations can spread through countries quickly, impacting potential economic activity.

We are heading into the last month of another difficult year with growing economic momentum. Following the economic shutdown in 2020 and the loss of eight million jobs, parts of the economy have been slow to reopen, including hospitality, travel, leisure and entertainment. In October, total nonfarm payroll employment rose by 531,000, and the unemployment rate fell to 4.6%, according to the U.S. Bureau of Labor Statistics. However, there are still 1.7 million workers out of work since the start of the pandemic.

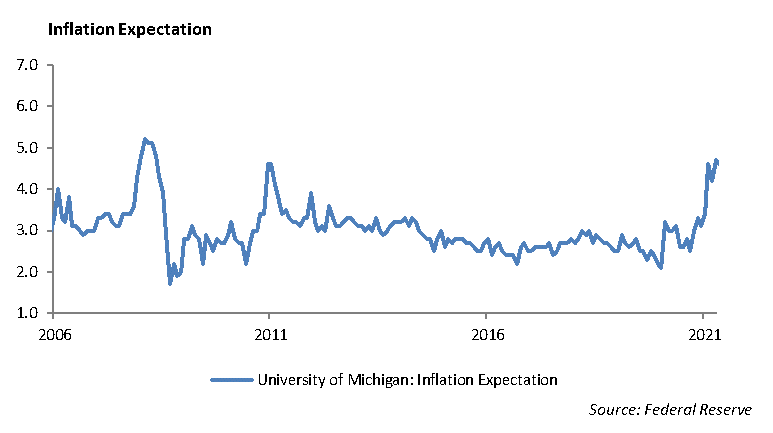

Since the first quarter of 2021, the pace of inflation measured by CPI has increased to 5%. The Federal Reserve has labeled the spike in inflation as transitory. They also indicated that employment growth is the policy priority, and they plan to maintain a level of patience with inflation. The increase in the rate of inflation is underscored by the continued supply chain disruptions, chip shortages, rising raw material prices and increased wage growth. The Fed could risk a policy mistake if they continue to treat inflation as transitory and minimize its sustained presence in the market.

Investment Expectations

For investors limited to long-only asset allocation, including stocks, bonds, and cash, the world may feel a little claustrophobic. The Fed has signaled a clear end to its generous monetary policies, which have supported the capital markets through the economic challenges cause by the pandemic over the past two years. They have signaled a long-term initiative to push interest rates higher. Domestic equities trade at excessive valuations of 34 times earnings, the second highest Price/Earnings multiple in history. Allocating the portfolio only to overvalued stocks and bonds with skinny yields feels limiting. Increasing the cash position may feel safe over the near term; however, with the rate of inflation near 5%, the buying power of the long-term cash position will erode over time.

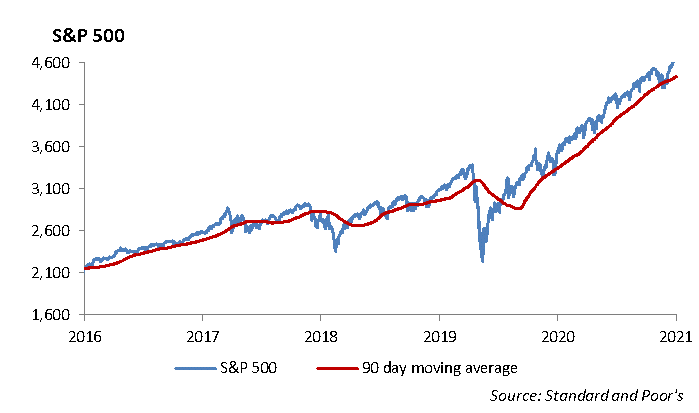

History illustrates that rising rates is not a great catalyst for rising stock prices. Over the period December 2015 to December 2018, the Federal Reserve raised the Fed Funds rate nine times from a market yield of 0.14% to 2.40%. Over that same period, the S&P 500 increased from 2043 to 2485, representing an annualized rate of return of 7.21%. The annual growth rate of the S&P 500 over the past two years is over 22%.

We expect the Fed will error on the side of accelerating its withdrawal of monetary stimulus sooner and that we could see an increase in the Fed Funds rate as early as June of 2022. This assumes that the Omicron variant does not get a grip on the global economy and force lockdowns which would impair economic growth similar to 2020.

Earnings comparisons year-over-year will begin to decline which will make earnings comparisons more difficult next year. Rising wages and raw materials, compounded by supply chain and inventory disruptions will have a negative impact on margins. In addition, the inability to completely pass on rising costs to consumers will negatively impact profits. It is setting up to be a tough year for the performance of domestic equities.

Investment Themes for 2022

Managing portfolio assets with the level of uncertainty and risk in the markets today requires thoughtfulness, discipline and intentionality of execution. Each year we attempt to establish some “guard rails” that help to serve as directional themes to help investors think through as they contemplate risk and potential return on their investment portfolio. Below is the initial outline for the investment themes we are developing for 2022.

- After five years of solid investment returns, return expectations for risk assets will be significantly lower.

- U.S. – China relations will take one step toward normalizing; however, divergent growth paths for China and the U.S. will continue. China will continue its military buildup to compete as a world super power.

- Supply shortages will begin to ease next year; however, a heightened level of inflation will be a challenge for investors through the year.

- Central banks of developed countries will increase short term interest rates.

- Economic growth in China is allowed to slow in order to digest its excessive debt.

- Stretched valuations in the equity markets, renewed focus on income in 2022.

- Fed Monetary policy moves to increased interest rates sooner than the market expects. With the Fed withdrawing its massive monetary stimulus, expect a shift in leadership away from growth and momentum stocks to more value-oriented stocks.

Equity

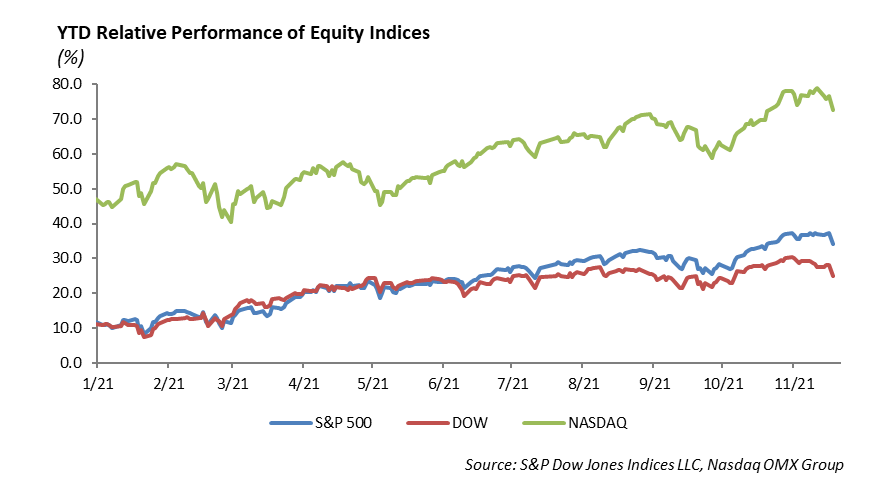

The equity markets sold off last week, with most of the damage coming on Friday due to the disturbing news around Omicron, the new variant of Covid that may prove more disruptive to the global recovery than other variants. Every major equity index traded lower with the S&P 500 falling -2.20%, the Dow falling -1.97%, and the Nasdaq dropping -3.52%. Vaccine stocks and stay-at-home companies benefited from the news of the Omicron variant. Stocks such as Moderna, Pfizer, and Zoom were the biggest movers on Friday. Cruise lines were among the hardest hit stocks as Carnival, Norwegian, and Royal Caribbean all fell over 10%. Airlines stocks were also punished quite severely as stocks like United Airlines fell almost 10% as well. Although it is very early, the symptoms of the new variant have been described as mild.

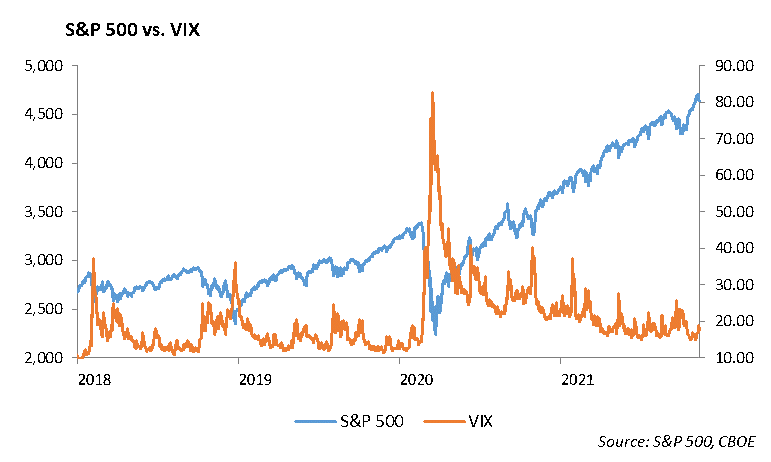

As we head into year end, we are expecting an increase in volatility, which could weigh on markets. The VIX has traded higher over the past month from 16 to 23. The move higher in the level of the VIX is indicative of the higher buying of put options as investors build downside protection into portfolio structures.

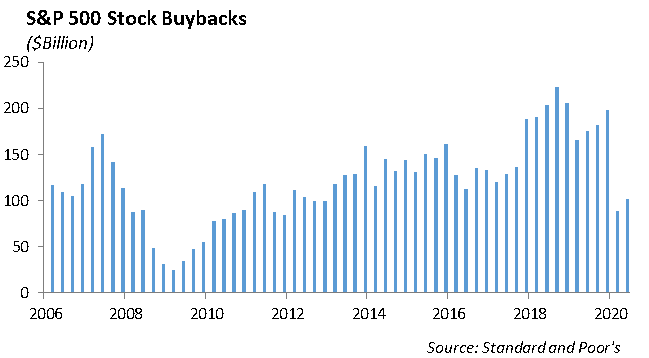

Flush with cash, we expect an increase in the level of stock buy backs in 2022.

Fixed Income

The calm of a short trading week came to an abrupt end on Friday as the fear of the spread of the Omicron virus, a new strain of the Covid virus, forced a shift out of equities and into bonds. On one of the lightest trading days of the year, the “risk off” trade resulted in yield on the 10-year U.S. Treasury to decline 16 bps in one day to a yield of 1.47%. Credit spreads widened as well. Investment grade spreads were roughly 10 bps wider and high yield spreads 20 bps wider on Friday alone.

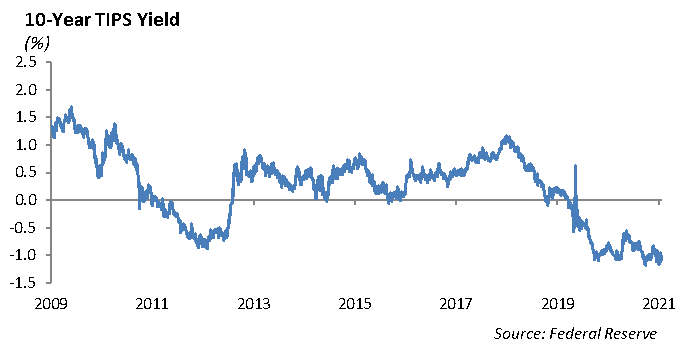

With the rate of inflation accelerating to 5%, the breakeven yields on TIPS has increased sharply by more than 7 basis points and is trading to around 2.72%. The yield on TIPS securities is tied to expectations on changes in consumer prices, which have historically exceeded the rate of inflation which the Fed targets by roughly 40 basis points.

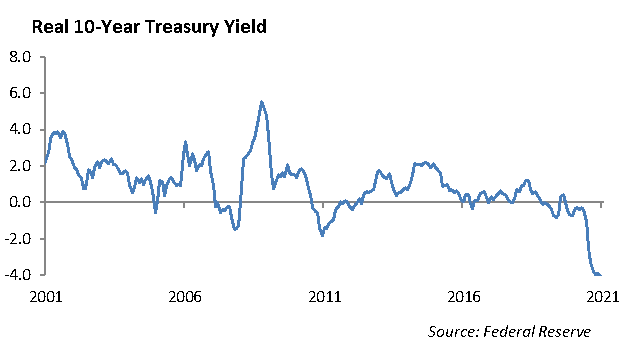

The spike in inflation has resulted in a sharp decline in the real yield in U.S. fixed income securities. We expect negative real rates will persist through next year as our outlook for inflation remains elevated above 3%.

Over the second half of this year, we have been moving up in quality across our fixed income portfolios given tight credit spreads and expectations for a shift in the tone of Fed monetary policy. By de-risking portfolios in periods where valuations are stretched, we have the opportunity to add to risk when markets sell off. The Covid virus is something markets will be forced to contend with for the foreseeable future. For these reasons, we have remained short the duration of the benchmark in order to reduce overall volatility of our fixed income portfolios. We expect liquidity will be more and more difficult the closer we get to the end of the year.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management