With the rate inflation running over 5%, will the Federal Reserve keep interest rates low?

In our opinion, the answer is no, they will not. Since the Financial Crisis, the Fed has longed desired a scenario of economic growth accelerating above 2.5% and inflation tipping over 2%. Now, with inflation running at a solid 5% on a trailing twelve-month basis, dislocations in major supply chains, commodity prices rising and wage pressure in many sectors, the Federal Reserve should be getting more serious about tightening monetary policy. Persistently low interest rates will effectively provide more stimulus to an economy that no longer needs the boost.

The demand side is strong. The consumer is strong. Corporate sector is strong. Housing is strong. The dislocation in the market is due to supply disruptions. In October, the Consumer Price Index for All Urban Consumers rose 0.9 percent on a seasonally adjusted basis; rising 6.2 percent over the last 12 months, according to the Bureau of Labor Statistics.

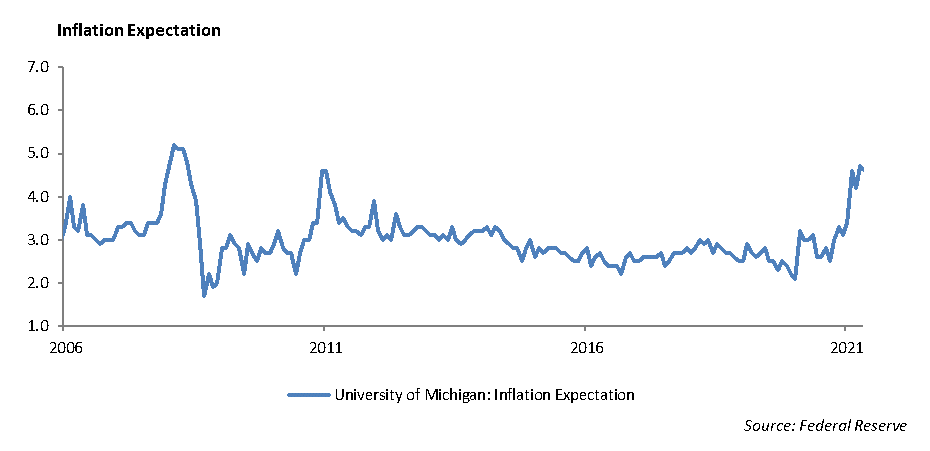

According to the University of Michigan survey, inflation expectations one year ahead are running at 4.8%, its highest level since 2008. A sustained high rate of inflation will negatively impact consumer behavior, business investment and ultimately living standards.

In addition, wage pressure persists around the country Increasing contributing to the rise in inflation. The Wall Street Journal reported last week that HCA Healthcare, one of the largest hospital chains in the country, increased its pay to nurses in order to remain competitive in the labor market.

The Catalytic Converter

We have held to the belief that there are societal indicators that reflect the current state of economic activity. While partially refuted by a Congressional Research Report in 2011, we believe there is a correlation between violent and property crime rates, the unemployment rate and economic downturns.

One consequence of the rise in commodity prices today is the growing theft of catalytic converters from the under belly of your car. The catalytic converter is an exhaust emission control device located near the tail pipe of gasoline-powered vehicles. Thieves crawl under the vehicle and remove the catalytic converter, often in a large seize of vehicles. The converters contain precious metals, including platinum and rhodium, which thieves then sell to scrap metal dealers.

The Federal Reserve

We have a new Chairman of the Federal Reserve. Well, he’s actually the old Chairman. Yesterday, President Biden reappointed Jerome Powell to another term as Federal Reserve Chairman and lifted Lael Brainard to Vice Chairman.

Chairman Powell leans to the dovish side and has been more liberal with monetary policies as a means to stimulate economic growth and promote full employment. With the recent pesky spike in the rate of inflation, we expect the Fed will shift to tightening policy faster than expected. We are looking for a 25 basis point increase in the Fed Funds by June of 2022.

The Economy

Retail sales jumped 1.7% in October as consumers accelerated their spending heading into the end of the year. The increase in sales at U.S. retailers alludes to a strong holiday shopping season and a pick up in the rate of economic growth for 4Q 2021.

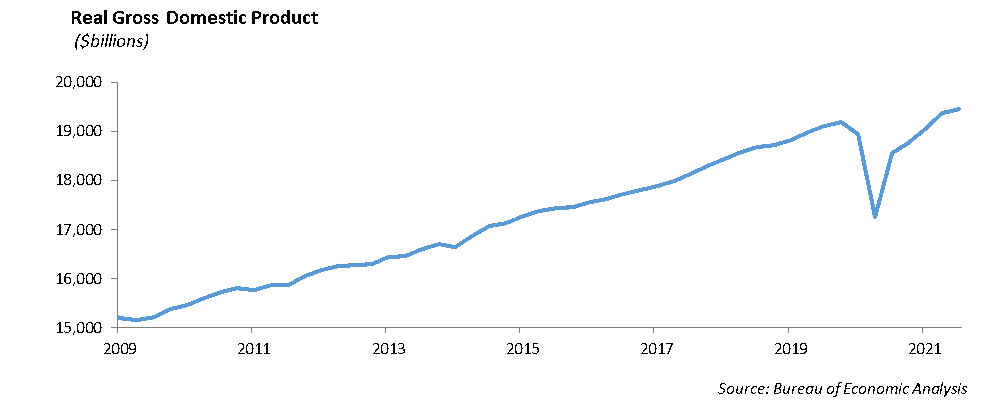

The U.S. economy, measured by real gross domestic product (GDP), expanded at a mere rate of 2% annualized in 3Q 2021, according to the Bureau of Economic Analysis. This represents a significant deceleration from the 6.7% GDP growth in 2Q 2021. In addition, it represents the weakest growth rate in the economic recovery following the pandemic. The deceleration is the result of a decline in government stimulus, combined with a surge in COVID-19 cases and global supply constraints. As a result, personal consumption growth declined sharply from 12% in Q2 to 1.6% in Q3. Spending on goods declined and services decelerated, led by food services and accommodations. The decrease in consumer goods was prevalent in the auto industry, as there are few cars on auto dealer lots for consumers to buy. In addition, the decline in residential investment helped to suppress growth.

Equity

Covid cases continue to accelerate across Europe and Asia. Supply chains are once again stressed. The rate of Inflation is outpacing wage growth. Despite these facts, investors continue to pour money into stocks. The S&P 500 is now up over 25% year-to-date. The NASDAQ 100, once a laggard this past year, is now outperforming other indices, up 28% year-to-date. Valuations are at historical highs, yet investors seem to be willing to look past the excessively high implied growth that are priced in the market. The S&P 500 is currently trading at 33x this year’s earnings and 26x next year’s earnings. Earnings are expected to grow by 17.5% next year, setting markets up for a high bar that will be difficult to surpass. In reality, markets appear to be priced to perfection, already discounting future growth. Therefore, forward looking returns are low, leading to an asymmetric risk/return profile. For our portfolio strategies, the story remains the same, we continue to reduce risk across our portfolios.

Finding a safe haven within the markets has proven to be difficult over the past several years. Value has underperformed growth for over 10 years. When we dissect value, however, it seems that performance is largely driven by the fact that Value strategies are allocated to the financial sector at twice the weighting of the S&P 500. Low Volatility strategies are over weighted to interest-rate-sensitive sectors, such as Telecom and Utilities.

Globally, developed markets continue to lag the United States. Japanese stock markets are up 3.5% and Europe is up 18%. Emerging markets have had a difficult year, largely due to the negative returns out of China. Looking forward, we continue to believe that the best investment opportunity from both a growth and a valuation perspective is China. Europe and Japan will likely be plagued with structural and demographic headwinds for the foreseeable future. While the U.S. currently looks like the brightest spot across the globe, we believe it is unlikely that the U.S. maintains its economic dominance over the next 10-years.

Fixed Income

Interest rates have largely remained range bound since the beginning of March, when the rate on the 10-year U.S. Treasury hit 1.70%. A shake up at the Fed is now firmly off the table. The Fed plans to begin tapering its balance sheet in December by $15 billion per month. Given that the Fed’s balance sheet now sits at over $8.5 trillion, the so-called “tightening policy” seems immaterial. We believe that the Fed will be forced to raise short-term interest rates well above 2% to truly begin tightening monetary policy. This initiative will prove to be very difficult as the Treasury is set to reduce issuance considerably over the next year. These two policy moves would prove to be contradictory and would minimize the effectiveness of monetary policy. Regardless, inflation is proving to be real and sustained, but the Fed may have found themselves in a negative feedback loop on monetary policy, with very few levers to pull.

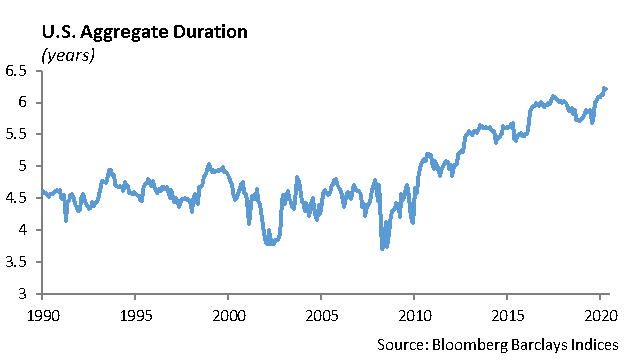

With interest rates historically low, it should be no surprise that both the U.S. Treasury and corporate America have been issuing more and more long-term debt relative to short-term debt. As a result, there has been a substantial lengthening in the duration of fixed income indeices. The Bloomberg U.S. Aggregate index duration has extended from 5.6 years to 6.7 years over the past year alone. The duration on the index remained range bound around 4 years from 1998 until 2011. Since then, the index has lengthened. The Bloomberg Corporate Index has a duration of 8.7 years. The longer duration means that investors buying index funds continue to take on more and more interest rate risk, while at the same time, the risk of rising interest rates is increasing. Many investors do not realize they are taking on this type of risk. Given how low rates are currently, returns on fixed income assets are likely to remain low. We prefer short duration fixed income strategies within our asset allocation in order to reduce interest rate risk and protect principal. Until we see broadly higher interest rates, we do not believe investors are adequately compensated for taking on additional duration risks right now.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management