The Economy

With the number of Covid cases accelerating to record high levels, we are at the intersection of the escalating pandemic and the rush to get the first vaccines delivered. Around the world, countries and cities are ramping up efforts to control the spread of the COVID-19 virus as pharmaceutical companies are racing to get vaccines distributed. Germany is shutting down its economy, which will likely push the country into a recession this winter. South Korean Prime Minister Chung Sye-kyun is fighting against a third wave of COVID-19 infections as his government considers increased social restrictions to contain the surge in outbreaks. In the U.S., New York City is once again closing all in-service restaurant dining, and downtown Chicago is a ghost town.

After proving that workers can operate effectively out of its New York headquarters, Deutsche Bank is planning on moving nearly 2,000 people out of its Manhattan office to cities that are cheaper.

John le Carré dies at 89 years old – author of The Spy Who Came in from the Cold and Tinker Tailor Soldier Spy.

Brexit

I can hear my teacher saying “You’ve had all semester to finish the paper,” as I struggle to cram it in during the final week of the semester. Likewise, the U.K. and European Union have had three years to put together a workable deal for Brexit. We have said all along, if there wasn’t an apparent plan near the beginning of negotiations, a Brexit deal was not going to happen. Under the current accord, Britain’s transition deal ends on January 1st and a deal with the European Union must be in place. The British government and European parliament are both prepared for emergency meetings prior to Christmas if legislation needed to be passed. The major sticking point continues to be the design and implementation of a system to ensure fair business competition between the U.K. and the E.U. companies.

Equity Valuation

DoorDash and Airbnb showed stunning performance at their IPOs last week as stock prices surged in excess of 85% on the first trading day. This price movement is illustrative of this year’s rally in technology stocks, which has been largely driven by stimulus and expectations for a recovery. The rally has pushed valuations of stocks to elevated levels. DoorDash, which has yet to show a profit, debuted at $182 per share, which was up 78% from the IPO price. At opening price, the company was valued at about $70 billion. The only two restaurants with higher market caps after its IPO were McDonald’s and Starbucks. Airbnb followed a similar trend opening at a price of $146, well above its IPO mark of $68. It ended the day at a valuation of $87 billion, surpassing the market capitalization of Booking Holdings.

Assuming trailing 12-month earnings on the S&P 500 of $98.80 and the S&P 500 trading at 3682, the trailing 12-month P/E ratio of 37.27x is near its highest level since the dot-com bubble in 1991. If we assume a forward 12-month earnings of $155 of the S&P 500, the P/E ratio is near 23.75x.

We expect the following two issues as a result of the surge in valuation. First, we expect returns on the S&P 500 will be low single digit given the elevated level of stock prices, unless earnings growth accelerates next year. And, if expected earnings disappoint, the downside risk to the market is likely greater than any upside opportunity for 2021. Second, we expect a shift in earnings-growth drivers from technology companies to companies that are rebounding from the re-opening of the economy following the pandemic.

Beijing has ambitions for Chinese pharmaceutical companies to become a major global distributor of coronavirus vaccines. Bahrain has become the second country to approve a coronavirus vaccine developed by Chinese state-owned group Sinopharm, following United Arab Emirates decision to “register” one of Sinopharm’s vaccines. This is consistent with the country’s initiative to compete on the world stage with the United States and Europe in manufacturing, technology and pharmaceuticals. Sinopharm’s vaccine, which was rushed to market, has a reported 86% effectiveness rate.

Equity

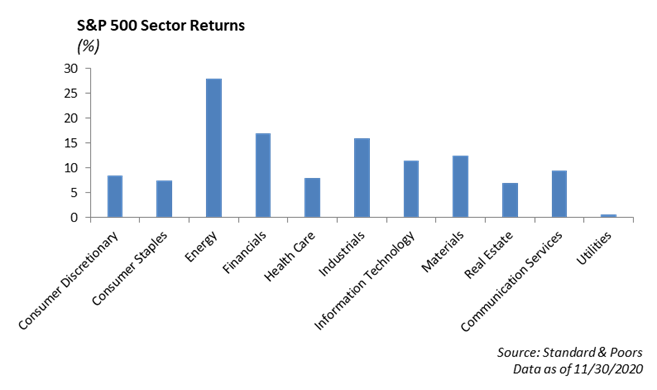

With the vaccine beginning to be distributed, previously beaten down sectors have begun to flourish. December has kicked off to a solid start for every index, but the recovery plays have led the month. Most S&P sectors are positive for the month, and Energy is the best performer. Over the last month, Energy is up 20%, but still down -30% year-to-date. Financials and Industrials are both up 5% as well. Earnings growth has spiked, with a record number of companies raising guidance. Additionally, the sector rotation and broad strength has taken some of the pressure off of the mega-cap stocks that initiated the comeback.

Disney [DIS] announced a few updates during their investor day, sending shares up 14% on the day and hitting all-time highs. Disney+ now has 87 million subscribers, a 14 million increase from their last quarter update. Disney is also raising the price of its service by $1, up to $7.99 per month. The company announced more than 100 new movies and shows, 80% of which will be added directly to Disney+. They expect to see 230-260 million subscribers by 2024, breaking all expectations. We continue to believe in Disney’s strategic plan, and we believe there is more upside ahead.

Fixed Income

This past week was the final push of liquidity for fixed income markets ahead of the holiday season. Wall Street notoriously begins to shut down in the two weeks heading into year-end, leaving a gap in prime broker balance sheets. More than $20 billion in new issuance came during the week, which was led by financials making up 87% of issuance. Less than $5 billion in issuance is expected next week. Money managers are clearly stepping back as well. Corporate new issues did not trade well in secondary markets. Two CLOs priced late in the week. These deals were supposed to price early in the week, but after weak demand, they were forced to delay them and did not fully subscribe some tranches. We have seen spreads on all fixed income asset classes tighten dramatically, the first signs of investors pushing back on unfavorable valuation and compensation for risk.

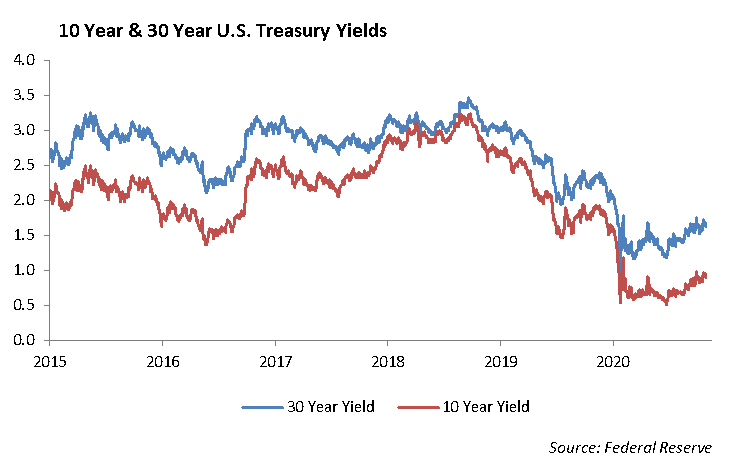

Despite all of the commentary that rates are destined to head higher, U.S. Treasury rates failed to climb after hitting 1.75% on the 30-year yield. After hitting that upper bound, it quickly fell -11 bps to end the week at 1.64%.

We have long believed that U.S. rates would remain range bound over the near term, despite increased economic growth. As we enter a new year with a reshuffled political cast, the questions are – what fiscal and monetary changes will take hold, and how will the market be impacted? Increased debt, yield-curve control, and a tighter bond between Washington and the Fed could have a material impact on the future of U.S. interest rates. We continue to believe that while stimulus could lead to some short-term spikes in interest rates, their path will inevitably trend downward toward zero.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2020 Winthrop Capital Management