Top Five Stock Picks

With the S&P 500 trading near 39 times earnings, equity valuations are extended. This makes it more difficult for investors to identify stocks that have the potential to post the growth rates we have seen over the past four years. Here are our top five stock ideas as we head into the remainder of 2021.

Microsoft [MSFT]

Microsoft Corporation has been a long term position in both our Large Cap Blend and Focus Growth portfolios. Microsoft is in the business of developing and supporting software, services, devices, and solutions. It operates through three business segments: Productivity and Business Processes; Intelligent Cloud; and More Personal Computing. We believe the Intelligent Cloud segment is one of the fastest growing segments. This segment includes the public, private, and hybrid server products and cloud services which power businesses. The company operates at 68.9% gross margins and 36.5% net operating margins. The company is expected to earn over $7.90 per share this year and $8.50 next year. At a current price of $300 per share, the company trades near 35.2 times earnings, in line with the S&P 500. Microsoft has a capitalization of $2.25 trillion.

Alphabet [GOOGL]

Alphabet, Inc. is a holding company engaging in the business of acquisition and operation of different companies. It operates through the Google and Other Bets segments. The Google segment includes its main Internet products, such as internet ads, Android, Chrome, hardware, Google Cloud, Google Maps, Google Play, Search, and YouTube. The “Other Bets” segment consists of businesses such as Access, Calico, CapitalG, GV, Verily, Waymo, and X. The company has a leading position in internet search and has seen significant growth during the pandemic. The company operates at 53.5% gross margins and 22.5% net operating margins. Currently trading at $2992 per share, the company could earn $100 per share next year, which puts the stock at a 29.9 times earnings, a discount to the S&P 500.

Tencent [TCEHY]

Tencent Holdings is the Chinese-based holding company of gaming, music, video, financial technology, social media, and overall consumer market place. Tencent dominates China’s online marketplace in terms of revenue and traffic volume, with the majority of their businesses ranking in the top three user base across China. While volatility is currently heightened due to increased regulations from the Chinese government, we believe companies such as Tencent are too important to the Chinese government in its plans to grow globally. Ultimately, we believe that China will not destroy largely successful companies, such as Tencent, for the sake of the Party. Tencent stock has declined -40% from its 52-week high and is still trading near its 52-week low price of $53.47. We expect earnings in 2021 to come in at $12.00 per share, leading to a forward P/E ratio of 22x. With revenue growth topping 20% and margins at 25% and expanding, Tencent is a rare company with a strong business model, rapid growth and a very cheap valuation. We expect continued noise from Chinese regulators as the Party continues to exert its influence on Chinese technology companies.

PayPal Holdings Inc [PYPL]

PayPal is a highly profitable company that also offers growth potential in a portfolio. Transaction revenues are the majority of its revenues, as PayPal dominates the market for payment processing. With almost 500,000 companies using PayPal, the company has a 54% market share. Second is Stripe, with a market share of 19%. Of all its subsidiaries, Venmo is driving transaction growth. Venmo has the lowest fees compared to its competitors, and it has shown the ability to adapt to the shifting market, now allowing users to buy cryptocurrency. In the most recent quarter, Venmo processed $58 billion in total payment volume, well above expectations. In total, the company had 4.7 billion payment transactions and added 11.4 million new accounts to over 400 million active accounts. PayPal has a diversified stream of global revenue, with domestic worldwide revenue split equally. PayPal’s digital business has been accelerated by the pandemic. Additional catalysts for revenue growth include penetrating into new markets and adding new products that will expand its total market. In 2020, the company launched QR Code Checkout, Venmo Credit Card, and Cryptocurrency. We expect these new features will draw more new users to PayPal. PayPal is currently trading at $278 and up 20% this year. However, the company is still down over -10% from its all-time highs. With expected earnings near $6.00 per share, the company trades at 46.3 times earnings.

Pfizer Inc [PFE]

Pfizer has reinvented itself over the last year, offering an attractive opportunity for investment. The company’s first and second quarter earnings highlighted the impact that the vaccine had and will have on revenues, as many international companies will need vaccines, and booster shots will be required. Even without the vaccine, the company showed strength in its pipeline and remains very cheap, making it a great pick. The company has already raised revenue estimates from its vaccine to $34 billion, up from $15 billion. Pfizer expects to deliver 2.1 billion doses in 2021 and to manufacture 3 billion doses by the end of the year. Additionally, there is further penetration that will occur as many young people are not vaccinated, and demand remains high in the global market. Pfizer increased revenue expectations for 2021 after the company recorded revenues of $19 billion in the second quarter, indicating growth of 86%. Over $8 billion in sales came from the COVID-19 vaccine distribution. Excluding its COVID vaccine, revenues still grew 10% in the second quarter, due to the success of its oncology business segment, which grew 16%. Pfizer has a strong portfolio of blockbuster drugs, including Prevnar, Ibrance, Eliquis, and Xeljanz. All of these drugs bring in over $2 billion in revenues every year and have patent expirations that are over 5 years out. Furthermore, its pipeline includes over 30 drugs that are in Phase 3 trials. Revenues in 2021 are expected to be about $79 billion, with earnings of $4 per share. The company is valued at 11 times forward earnings, much cheaper than all of its peers. Fellow pharma giants, Johnson and Johnson and Merck, are trading at 14x and 18x forward earnings.

The Fed’s Tight Rope Walk Continues

The Federal Reserve continued its tight rope walk this past week with announcements from its Jackson Hole WY summer meeting.

In an effort to reassure investors and the capital markets, Fed Chairman Powell continued to indicate that the Fed could begin to reduce its asset purchase program as early as this year; however, it would be a long time before the Fed began adjusting short term interest rates higher.

The last thing the Federal Reserve desires at this point is to squash the recovery. He indicated that there is still much ground to cover in economic healing, and the Delta variant is a potential impediment to continued economic expansion.

Both the economy and the labor market have shown significant improvement. The demand side appears intact; however, there are supply disruptions negatively impacting the economy and forcing inflation higher. The personal consumption expenditures (PCE) index rose 4.2% last month, the fastest pace since 1991.

Fixed Income

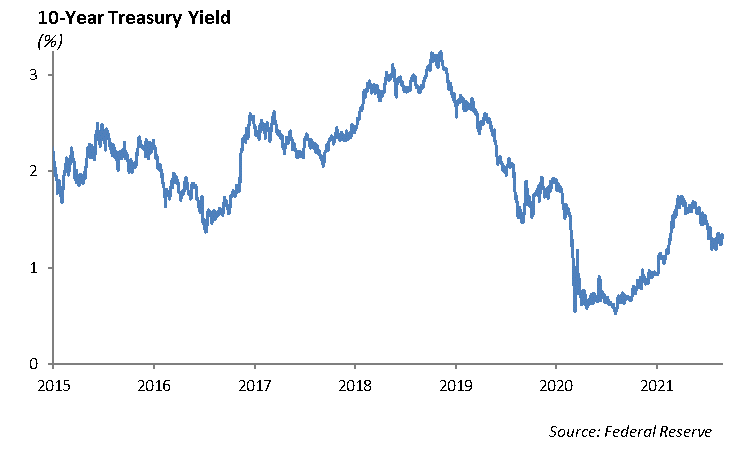

Last week, at the much-anticipated Jackson Hole Federal Reserve meeting, Fed Chairman Powell let markets know that tapering could begin in 2021. Despite this news, interest rates on the 10 year U.S. Treasury actually declined by over -4bps. While stock prices rallied, the bond market is demonstrating that they believe the Fed will not taper too aggressively in order to not choke the economic recovery and future growth. The pattern is consistent with history, as the curve is flattening by a combination of rising short-term rates and declining long-term rates. In other words, rising short term rates have a negative correlation to long term growth and rates.

Over the past several weeks, we have been navigating investment strategies to weather the headwind of rising interest rates for the fixed income allocation of our portfolio models. Historically, ultra-low interest rates combined with tight spreads have made it seemingly impossible to generate meaningful income in portfolios. Money markets essentially have a yield of zero, the Bloomberg Barclays U.S. Aggregate Bond Index yields 1.72%, and the Bloomberg U.S. High Yield Corporate Bond Index yields less than 4%. Investors are left to either extend duration, move down in quality, or both in efforts to increase yield. As more money flows into the bond market, there appears to be a negative feedback loop that is continuing to drive spreads tighter, particularly in high yield. We are growing more uncomfortable with the risk in the fixed income allocation across our models and believe we are in the seventh inning of this credit cycle. While we see pockets of relative value opportunities across shorter duration BBB and BB corporate bonds, we prefer moving up in quality in our fixed income strategies. One alternative is to look outside of the U.S. bond markets. In the emerging markets, the 10-year Chinese government bond yields nearly 3% with an A credit rating. We acknowledge that this is not the same as investing in domestic fixed income, but relative to 10-year U.S. corporates trading at 2.04%, there is a clear relative risk-to-reward value.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management