Just as the economy should be accelerating, it is beginning to show signs of slowing. The Covid-19 variant is hitting the U.S. and, combined with supply chain disruptions and labor market dislocation, is hampering efforts to re-open. The momentum in economic growth is petering out, resulting in several negative effects

- Third quarter earnings growth will likely slow. Earnings comparisons in the second half of 2021 are going to be more challenged as we move beyond the low bar set during Covid last year.

- Office vacancy rates in large cities are climbing. The vacancy rate in New York hit 18.7%, an all-time high in 2Q 2021 according to Newmark, as workers adapt to remote or hybrid work schedules. Small businesses that rely on people working in offices, including restaurants, dry cleaners, catering, and parking, are experiencing slow demand.

- Supply chains are still in disarray and will put pressure on corporate earnings.

- There is discussion about another federal rescue package for small businesses.

At current levels, equity markets appear to be priced to perfection graciously discounting good news while ignoring the growing risks, slowing revenue growth, and pressure on operating margins.

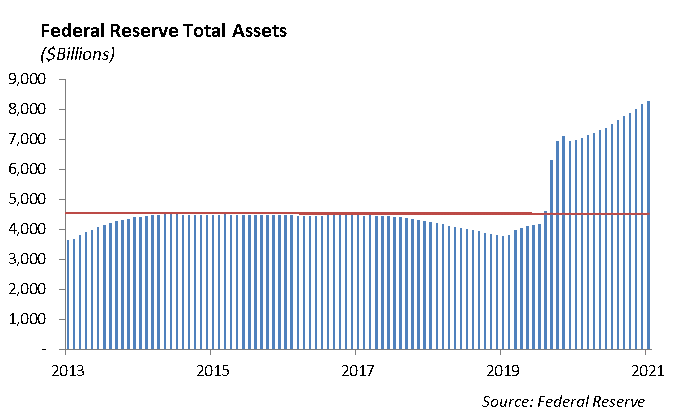

Easy monetary policy combined with generous fiscal stimulus is a cocktail for rising asset prices. Over the past four years, we have had $4.5 trillion in monetary stimulus and over $4.8 trillion in fiscal stimulus injected into the economy and capital markets. The Democrat priorities are pushing the $1 trillion bipartisan infrastructure bill and a $3.5 trillion budget bill through congress. Corporate and individual taxes are going to increase in order to help pay for the aggressive spend. This will be another source of uncertainty for the markets to digest.

If the fiscal spending package is not passed, a major source of fuel for the capital markets for continued growth will be removed. In addition, the first sign of normalization in monetary policy should occur before the end of the year as the Fed begins to reduce its monthly bond purchases through its quantitative easing program. We don’t expect this to be an issue for the market since it’s been widely telegraphed.

Many of the extended benefits to unemployed workers have now expired, including rent relief, a moratorium on student loan payments and extended unemployment benefits. In conjunction with schools re-opening with in-person classrooms, this should provide a catalyst for more people to reenter the labor market and expect to see results in the next 45 to 90 days.

Fixed Income

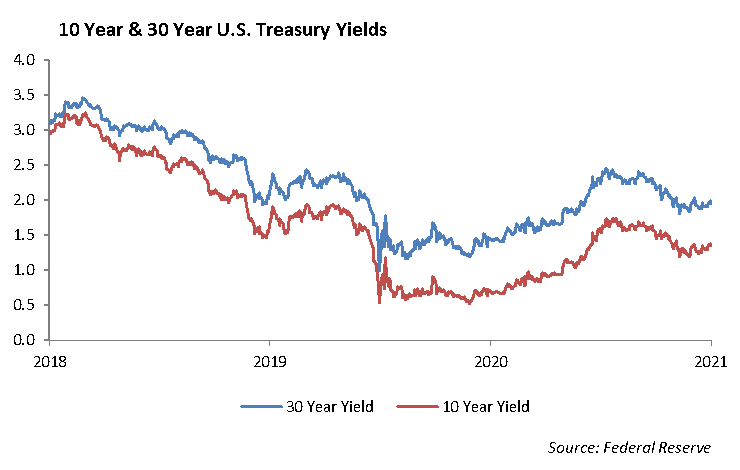

Over the past several weeks, we have seen U.S. Treasury auctions perform extremely well. Last week’s 30-year auction was no exception as demand from foreign buyers remains higher than normal. Rates across the curve were down over -5bps after auction results, and the 30-year U.S. Treasury rate ended the week below 1.90%. This was supported by weaker economic data, as the economy is showing signs of slowing much sooner than most expected. With economic growth slowing, it is unlikely that we will see any meaningful move up in interest rates, regardless of short-term inflation data.

Similar to the excessive valuations in the equity market, we are seeing extended valuations in the credit markets. Post pandemic, leverage ratios remain elevated, yet credit spreads across all ratings and durations are at historically tight levels. With interest rates remaining low, investors have been seemingly forced to chase any yield they can find. Even with last week’s heavy new issuance calendar, concessions were non-existent, and secondary markets continued to tighten. We may sound like a broken record, but we continue to reiterate that now is not the time to add risk to portfolios. We continue to de-risk portfolios by moving up in quality, shortening duration, and increasing cash. Considering all that is happening in the markets and economy, we are preparing portfolios for a potential storm at this point in time. Once riskier assets become cheaper, we will look to increase their allocation in our fixed income portfolios.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management