The current period feels like we are in the proverbial “calm before the storm.” The markets are quiet at elevated valuations, trading in a tight range. Bond yields are trending lower. The economic recovery appears to be running out of gas. Congress is trying to address the next round of fiscal stimulus wrapped up in a $3.5 trillion infrastructure bill. In addition, the Federal Reserve has begun its narrative around tapering this year, its process to withdraw monetary stimulus from the markets.

Over the past 18 months, the financial news has been dominated by the Covid-19 virus, including the massive push to control the spread, the rush to bring vaccines, and economic stimulus needed to support the crippled economy. Despite great progress, we have entered into a new stage of trying to reopen the markets and live with the Covid variant. We are in a cautiously optimistic period of getting kids back into the classroom, finding methods to gather the public for sporting events and entertainment, and encouraging workers to re-enter the labor market. We expect the equity market is vulnerable to negative news.

With slowing growth in China, growing geopolitical challenges, and Europe’s impaired economic recovery, there is no shortage of potential negative news, which could impact the markets. However, there is one issue that has our attention. We are focused on the brinksmanship playing out between the United States and China, with its increasing aggressiveness in the South China Sea and the potential threat to Taiwan.

Beijing has been cracking down on its technology companies, placing curbs on the use of video games, tutoring, and profits. The communist party is interested in aligning its entrepreneurs’ success with that of the government. The latest casualty is the China Evergrande Group, one of the largest residential construction companies in China. Fueled by massive debt and unable to meet its financial obligations, the company is on the brink of collapse and unable to pay its bills. The government is trying to curtail the heavy use of corporate debt to fund growth. The reality that China would allow the company to collapse, leaving massive apartment projects uncompleted, rippled through global markets Monday, as investors feared consequences would lead to additional failures, undermine financial stability, and weigh on China’s economic growth.

Equity Market Valuation

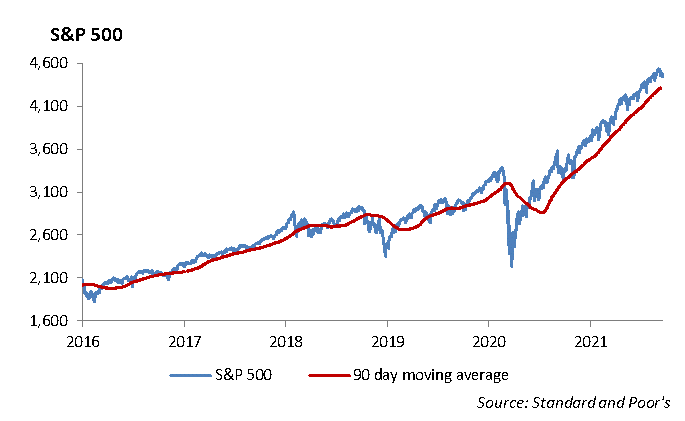

Assuming earnings on the S&P 500 of $134 per share, the S&P 500 is trading roughly at 34 times earnings at the current level of 4433. With earnings growth expected to slow from current levels, we expect to see more stock buybacks and dividend increases over the next two years. However, companies are going to be challenged over the next year with maintaining operating margins while navigating increases in labor costs, raw materials, and taxes.

- S&P 500 revenue growth for the second quarter of 2021 increased 9.64% on an annual basis.

- Companies experienced 94.7% growth in year-over-year Net Income.

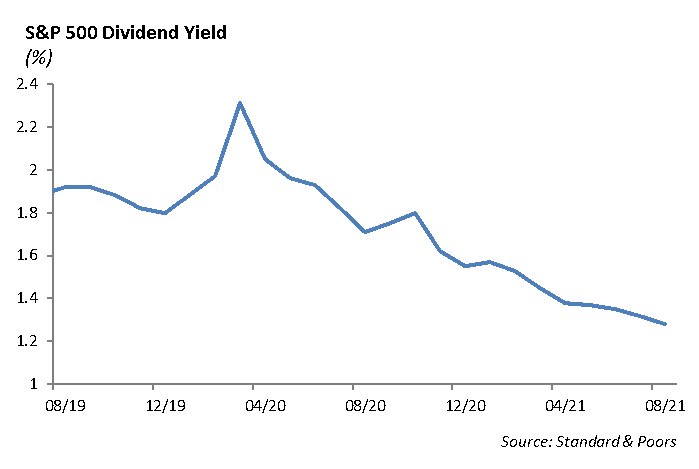

- The dividend yield of the S&P 500 has declined from 1.8% last November to 1.28% as of August 31st.

Equity

The S&P fell -0.57% last week ending at 4432. At the Monday open, the index is up 18% this year and is trading at levels that are just off of all-time highs. Over the last month, industrials, utilities, and materials have lagged the market, falling about -4% each. These sectors have also lagged on a year-to-date basis, as materials and utilities are two of the three worst performing sectors.

The consumer discretionary stocks continue to lead the way over the last month, rising 4% since the beginning of the month. Retail sales, which disappointed in July, came in strong over the last month as August gains of 0.7% easily beat estimates.

The Nasdaq is performing similarly to the S&P this year, as the Tech-heavy index is up 17%. The top five holdings in the S&P 500 index are Apple, Microsoft, Amazon, Tesla, and Alphabet. These stocks combined make up a stunning 40% of the index and contribute heavily towards performance. Year-to-date, Alphabet has carried the index, as shares have risen over 60%. Microsoft has also performed very well, rising almost 40% this year. Rounding out the top holdings, Apple is up 13%, Amazon is up 9%, and Tesla is up 4%.

This concentration undermines the implied diversification of a broad market index and creates added risk for investors. At some point, we expect a transition in the leadership of those stocks that performed well during the pandemic (the Big Five), to a new group of stocks that will lead the market though its next phase. When that happens, the performance of the S&P 500 will likely correlate with what the stocks of the Big Five are doing, and not necessarily reflect the performance of new leadership.

Fixed Income

With interest rates continuing their move lower across the globe, investors are likely asking themselves how bonds can fit into their portfolio. With equity markets seemingly in a perpetual bull market, it is easy to question risk management strategies in an asset allocation. Investors notoriously look at what they missed out on rather than the risk that was avoided. We have quickly forgotten about the -25% drawdown from the Covid pandemic and the -45% drawdown during the 2008 Financial crisis for the S&P 500.

While the Bloomberg Barclays U.S. Aggregate Bond index declined during both periods, it did so with much less volatility and outperformed stocks by over 20% in both cases. More importantly, returns were produced in an uncorrelated fashion. The U.S. Aggregate Index had a correlation of only 0.18% during the 1st quarter of 2020. In a proper asset allocation, this allows portfolio managers to reallocate fixed income assets into equity securities at lower prices and more attractive valuations. Over multiple market cycles, this strategy has proven to lead to outperformance on both an absolute and a risk-adjusted basis.

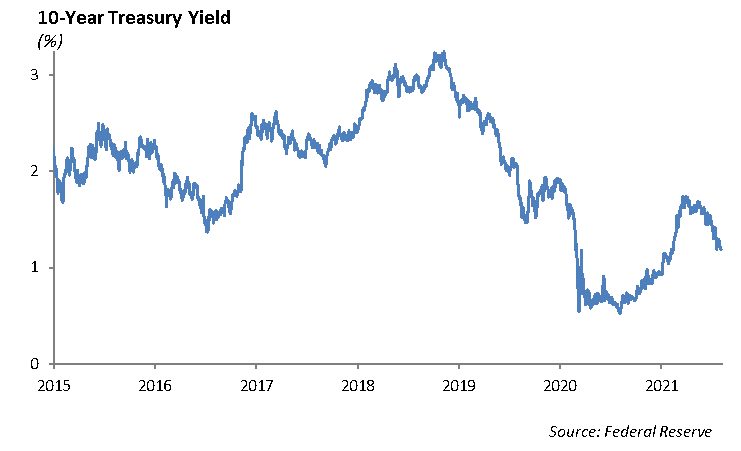

The 10-year U.S. Treasury yields 1.30%, and the corporate bond index yields 2.02%, meaning fixed income investors are realizing negative net yields given current inflation rates above 2%. While we are constantly seeking ways to put income into portfolios as portfolio managers and risk allocators, we more importantly realize the important role that fixed income plays in risk management. With equity valuations at all-time highs, and economic data pointing to a slowdown in the post-pandemic economic recovery, we believe an increase in risk management across asset allocations is more important now as ever.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management