Investing is all about digging beyond the headlines in the financial press. When you peel back the layers of the capital markets, there is always more detail to uncover, either confirming your investment strategy or allowing you to shift tactically. Listen to this week’s episode as we acknowledge that the capital markets are very intertwined amidst recent events and discuss the tactical moves we’re making in portfolios as more economic data is uncovered.

The Economy

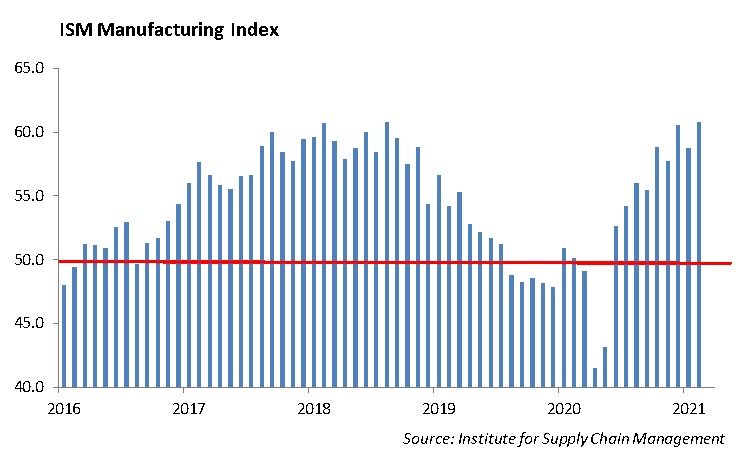

The domestic economy is beginning to show signs of acceleration as we expected for 2021. We are seeing improvement in manufacturing and consumer sectors of the economy.

Last week, the IHS Markit Flash US Manufacturing PMI edged up to 59 in March of 2021 from 58.6 in February. The improvement in operating conditions was the second-fastest since April 2010, underscoring strong demand. However, supply chain distributions are impacting costs, and a lack of raw materials is contributing to pressure on vendor performance. At the same time, an increase in new business accelerated to the sharpest since June 2014 while job creation remains strong.

Business confidence remained upbeat, as firms expect strong demand will support a rise in output over the next year amid stronger new order inflows and an expectation for an end to the pandemic.

Government programs and financial assistance have provided strong support for the consumer sector. With the distribution of $1400 stimulus checks for qualifying citizens over the past two weeks, we expect consumer spending to accelerate heading into the second quarter of 2021. The $900 billion stimulus program in December of 2020 provided strong support for consumers, causing a sharp 10.1% increase in household income according to the Commerce Department. While February saw a -7.1% drop in household income, we expect that March and April will once again show strength following the passage of Biden’s Covid pandemic relief legislation. The relief package also provides additional $300 a week in enhanced compensation for unemployed workers. We expect demand will remain strong through the year.

We remain focused on whether the expected sharp increase in demand will push inflation up. The anticipation of stronger economic growth is pushing bond yields higher. At this point, we expect a shortage in labor in the fourth quarter as the service sector ramps up hiring, which will put short term pressure on wages. However, we do not expect this to lead to sustained inflation.

China

Biden’s team recently met with delegation from China covering issues ranging from trade to human rights, and once again, we are left with the impression that the US-China relationship is in gridlock, similar to a cargo ship blocking the Suez Canal. The trade tariffs on Chinese imports implemented by the Trump Administration will remain in place for now. This makes it more difficult for China to sell goods in the United States, and more expensive for U.S. consumers to purchase goods and materials from China.

In retaliation to H&M’s comments six months ago, the company has come under criticism in China. H&M distanced itself from cotton sourced from China’s Xinjiang region due to forced labor in the manufacturing of cotton. As a result, authorities in China have removed H&M from internet searches and apps, so there is no longer any reference to the company operating in China. In addition, several Chinese celebrities have severed deals with the Swedish company.

China’s form of authoritarian capitalism combines the ability to own private property and the functioning of open market forces with repression of dissent, restrictions on freedom of speech and an electoral system with a single dominant political party. China is growing more aggressive in asserting its form of capitalism and leadership to the rest of the world.

The Securities & Exchange Commission reiterated its warning at the end of the quarter that it will require the accounting firms doing financial audits on Chinese companies to let U.S. regulators review the financial audits. Foreign companies have three years to comply, and the penalty for non-compliance will be ejection from exchanges. At the same time, China’s government widened its crackdown on the country’s largest internet corporations, fearful of their growing clout after years of relatively unfettered expansion. The result is that stocks selling into China are trading significantly lower, including Baidu, Alibaba, Tencent, and many are down over -10% for the year.

Equities

We believe two things are certain. First domestic stocks are trading at historically elevated levels. Second, because of the amount of monetary and fiscal stimulus pouring into the capital markets, stocks valuations will remain elevated over the next year.

Fixed Income

The move up in rates paused during the past week, as the rate on the 10-year U.S. Treasury declined by -10bps to 1.60% week-over-week. Over the past several weeks, the selling of U.S. Treasuries has been led by Japanese investors. Rate moves has predominantly happened during the overnight Japanese session as inflation fears have spooked foreign investment. The move is even more telling, given the fact that JGB’s continue to have a negative yield out to 10 years.

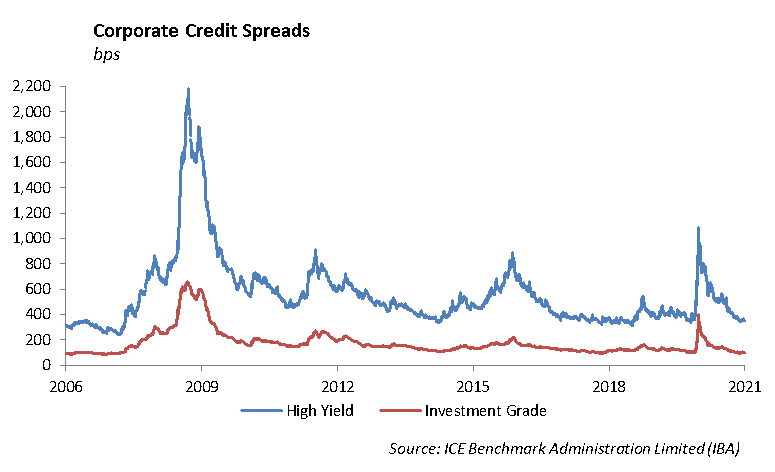

Investment grade and high yield spreads continued to remain tight during the week. New issuance picked up during the week, led by the recently downgraded Oracle. Oracle debt was issued 40bps wide of where bonds traded prior to moving to a BBB rating. Large cap energy was also broadly downgraded, but Exxon, Shell, Chevron, and BP all remained with at least an A rating.

Overall, spreads remain at cycle tights. With corporate debt levels and leverage at all-time highs, we are cautious investing in credit on the long end of the curve. We continue to invest into BBB credit on the short end of the curve but have continued to move up in quality out the curve. While there is further potential for spread tightening, the downside risk to spread widening has become more asymmetric.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management