Our base case for the economy hasn’t changed. We expect the vaccines will be effective at controlling the spread of the COVID-19 virus. We are at the intersection of the spread of the virus and the rollout of the vaccines, and the number of COVID-19 cases is declining. As the pandemic subsides, the economy will continue to reopen, including hotels, travel and leisure, conventions, and entertainment. While this is beginning to happen, we are a little surprised (and disappointed) that this summer’s concert schedule for this summer, which includes the Goo Goo Dolls, Billy Joel and Mercy Me, is being postponed again.

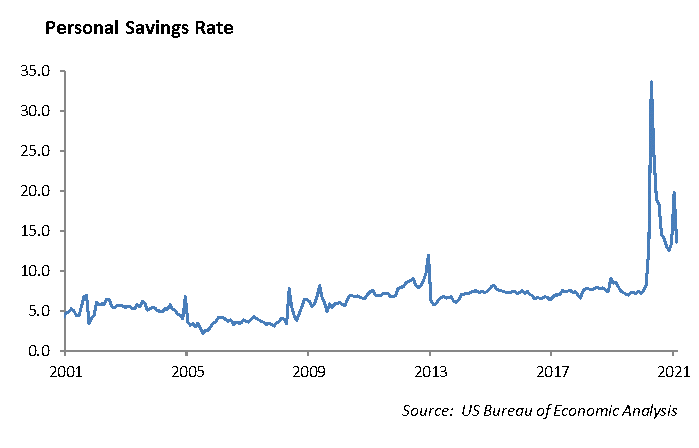

The recovery will benefit from pent-up savings during the pandemic shutdown. Because the travel, leisure and entertainment sectors were effectively closed, consumers didn’t spend as much money. Personal savings is fuel for an economic recovery, and during the past year, the savings rate increased substantially. Moody’s Analytics estimates household savings worldwide increased by $5.4 trillion by the end of the first quarter.

The Biden tax plan has weighed a bit on equity prices as investors digest its impact on their situation. Biden’s tax plan contemplates an increase in the tax bracket for wealthy individuals and corporations as well as an increase in the capital gains. Historically, equity markets move through short-term dislocations with changes to the tax code.

One of the keys to the economic recovery is the labor market. As the economy reopens, demand for labor will increase. Last week, initial jobless claims fell 39,000, bringing seasonally adjusted workers filing for jobless claims to 547,000, the lowest level since early 2020.

At the same time, home prices around the country have sky-rocketed. Median prices of existing homes rose as existing home sales dropped 3.7% last month. A confluence of factors, including moving out of downtown urban areas, the shortage of new homes for sale and the rapid increase in lumber prices, have combined to push home prices higher across the country. This speaks to the supply-chain disruptions in the economy.

We are facing a semiconductor shortage that is impacting auto production, laptops and PCs, and pretty much anything that uses a circuit board. We are expecting to see earnings misses as revenue declines resulting from supply-chain disruptions in certain companies, including Ford, General Motors, and Honeywell.

Europe

New York Times has a story this week that indicates the EU could allow vaccinated U.S. travelers into the country beginning this summer. A significant part of the economies of the southern European countries is supported by tourism. This is a huge step to moving the EU economy toward sustainable growth.

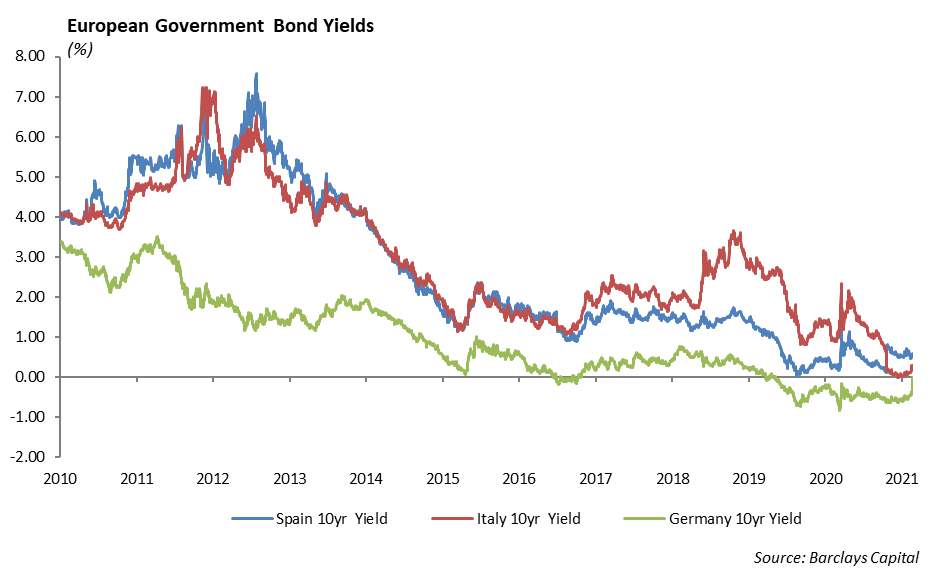

The European Central Bank (ECB) announced last week that it will maintain its current monetary stimulus policies. The EU is facing a resurgence of the COVID-19 virus due to an inconsistent rollout of the vaccine, which has kept large parts of the economy closed and, in some cases, cities in lockdown.

The ECB said last week that it would keep its key interest rate at -0.5% and continue its €1.85 trillion bond- buying program. The ECB is not ready to move away from its negative yield program. The credit direction of the larger European countries, including Spain, Italy and France, is generally negative. European banks, which are buying the bonds of these European countries, are saddled with the burden of this credit deterioration.

Equity

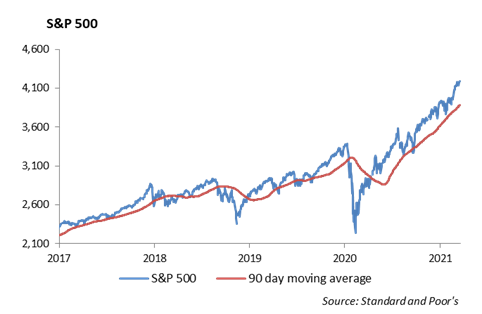

The markets continue to trade at all-time highs with the S&P 500 ending the week at 4180 last week. Earnings season continues its robust start, mirroring the strong economic data in the first quarter. Growth estimates for the first quarter have already begun to rise to a 27% growth year-over-year. This is up from the initial 20% expected bump. The number of companies raising estimates is also very strong. The season has just started, but of companies that have reported earnings, 83% have beaten estimates on sales and earnings. The highlights from last week include Johnson & Johnson, IBM, Netflix, and AT&T.

Johnson & Johnson [JNJ]

Johnson and Johnson reported earnings of $2.59 per share vs. $2.34 expected. The company reported $22.32 billion in revenue, which also beat expectations. The pharma business posted strong revenue of $12.2 billion in revenue, a 9.6% increase year-over-year. In addition, the company reported $100 million from its COVID-19 vaccine, which was briefly on hold as the CDC investigated the rare blood-clotting side effect. The consumer unit was down -2.3%, and its medical device unit was up 8% to $6.57 billion. J&J raised both earnings and revenue guidance for the year, and the stock was flat on the earnings release. We continue to hold JNJ as a pillar in our equity portfolios.

IBM [IBM]

IBM reported earnings of $1.77 vs. $1.63 expected. Revenue was $17.73 billion vs $17.35 billion. Revenue was up about 1% year-over-year, which is the first quarter of growth in the last year. Global Tech Services revenue was down -1% year-over-year to $6.37 billion. The Cloud and Cognitive Software division generated $5.44 billion, which was up 4% year-over-year and beat consensus. Systems revenue was up 4% and Global Business Services was up 2%. Shares were up 3% on earnings release and up 6% this year. This feels like the longest turn-around in corporate history.

AT&T [T]

AT&T reported earnings of 86 cents, a beat by 8 cents. Revenue was up 3% to $43.9 billion, which was a beat by $1.21 billion. Shares are up almost 4% after topping profit, revenue, and subscriber additions. HBO Max gained 2.7 million U.S. subscribers, bringing the total to 44 million. Worldwide subscribers totaled 64 million. Wireless subscriber adds beat estimates as well, with 595,000 vs. 270,000 expected. Cash from operations was $9.9 billion, up 12%, with free cash flow of $6bBillion. For 2021, the company expects revenue growth of 1% with free cash flow of $26 billion. AT&T’s challenge continues to be its ability to pay down its massive pile of debt while supporting its dividend and investing in its businesses.

Netflix [NFLX]

Netflix beat both earnings and revenue expectations, but a big subscriber miss sent shares down more than -8% on its earnings release. Earnings per share were $3.75 vs. $2.97 expected. Revenue was $7.16 billion vs. $7.13 billion expected. Global paid net subscriber additions were 4 million, which missed the 6.2 million estimate. Netflix subscriber growth drastically outperformed the market during the past year. However, competition remains high with Disney+, HBO Max, Apple TV+, Amazon Prime, and Peacock all battling for subscriber growth.

Fixed Income

Bond market volatility remained low during the week. The yield on the 10-year U.S. Treasury was relatively unchanged at 1.56%. Global yields remain low, with both German and Japanese yields negative out to the 10-year part of the curve.

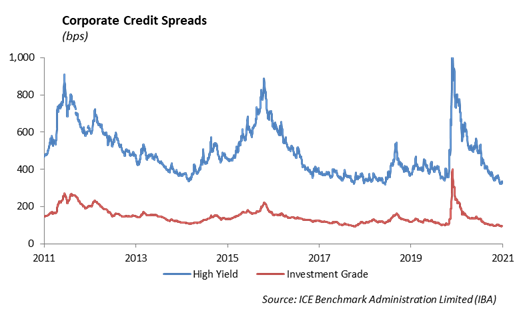

Corporate bonds continued their tightening cycle with volatility declining. Investment-grade spreads, at 90 bps, and high yield spreads, at 335 bps, are at 10-year tights. Building income into portfolios without taking outsized risk continues to be a significant challenge. We still believe BBB and BB credit is best utilized on the short end of the curve. With a steep yield curve and tight spreads, we prefer higher rated bonds on the long end of the curve. We have found that this is the best way to maximize yield, or income, while mitigating overall spread widening risk. Ultimately, the credit cycle remains on firm ground, and with a reopening economy, it is unlikely that we see any significant turns in credit quality in the near term.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management