The domestic economy continues to show strong growth with the U.S. Bureau of Economic Analysis posting first-quarter GDP growth of 6.4%. This reflects the continued recovery throughout the economy and the reopening of restaurants and entertainment following the pandemic. The strength of the recovery continues to be supported by the government’s response, through both fiscal and monetary initiatives.

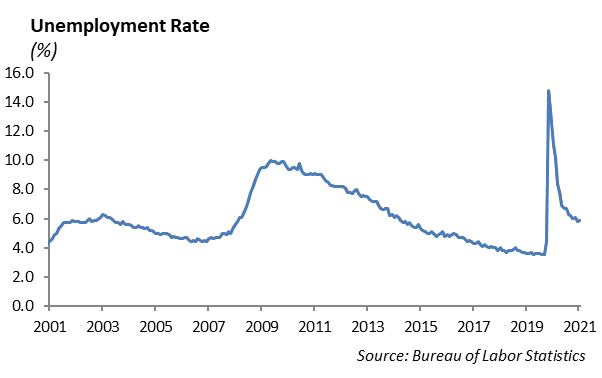

The labor market remains a critical factor to a sustained recovery and there has been significant improvement so far this year. Through the first half of the year, filings for weekly unemployment benefits have declined from 900,000 to nearly 370,000. The unemployment rate has remained around 5.9% and the June jobs report showed employers added 850,000 jobs, the largest gain in 10 months.

According to the Labor Department report, there were a record 9.2 million job openings in May and 9.3 million unemployed workers looking for jobs. As a result of the pandemic, a number of challenges are facing workers going back to work, including obtaining childcare, extended unemployment benefits that are making low-wage jobs less attractive, and remaining fears around the COVID-19 virus. While the job market is experiencing structural challenges getting people back to work, it is still very strong. Many of the impediments to getting people back to work will decline over the next quarter as schools move back to in-person learning and the enhanced unemployment benefits come to an end. We expect to see some increased wage pressure as incentives increase for a competitive labor market.

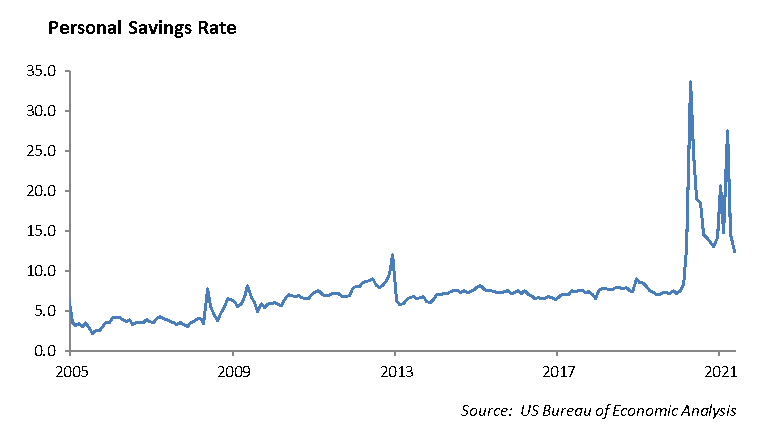

Employment drives consumption. The Consumer sector has been heavily supported by government assistance, including extended unemployment benefits, rent relief and student loan forbearance. However, much of this support is expected to end this quarter and will place more of a burden on the economy. Households increased savings to $2.5 trillion in their bank accounts through the pandemic, and we expect some of that to transition into consumption as the economy reopens, which will support continued growth in the second half of the year.

For the most part the recovery is broad based across the economy. The increase in first-quarter GDP reflects an increase in personal consumption expenditures, nonresidential fixed investment, federal government spending, residential fixed investment, and state and local government spending that were partly offset by decreases in private inventory investment and exports. The recent spike in oil prices, while not a major surprise, should not be a significant impediment to the economy. We expect oil prices to normalize late this year as OPEC figures out its production quota and U.S. shale production increases.

Equity

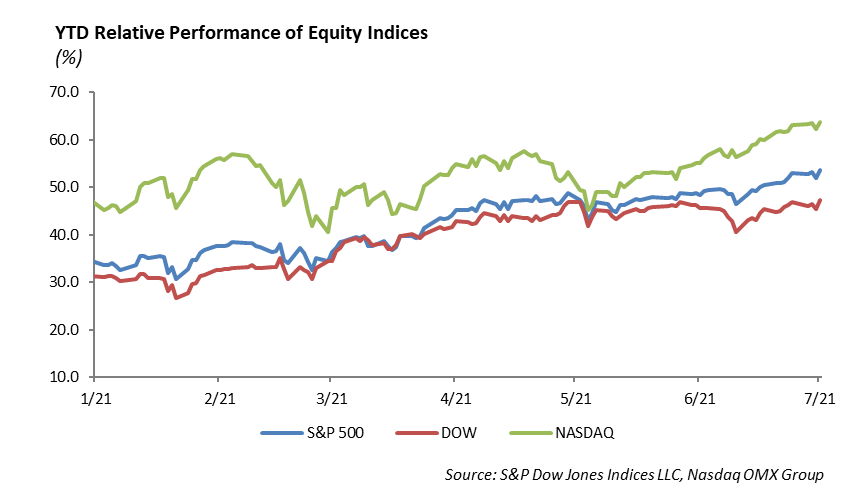

The S&P rose 0.40% last week and stayed at all-time highs. The Index was led by the Consumer Discretionary sector last week as Amazon’s large weight contributed to the positive performance. Energy and Real Estate continue to lead the S&P this year, up 40% and 26%, respectively. Staples and utilities are the laggards of the Index and are only up 3% for the year. The Nasdaq also rose 0.40% this week and is bordering on all-time highs at 14701. The Tech-heavy index is up 14% this year. Finally, the DOW was only slightly green for the week and is up 13% year to date. Second-quarter earnings are set to begin this week with Financials set to report. This includes Goldman Sachs and JPMorgan on Tuesday, Bank of America, Citigroup, and Wells Fargo on Wednesday, and Morgan Stanley on Thursday.

Fixed Income

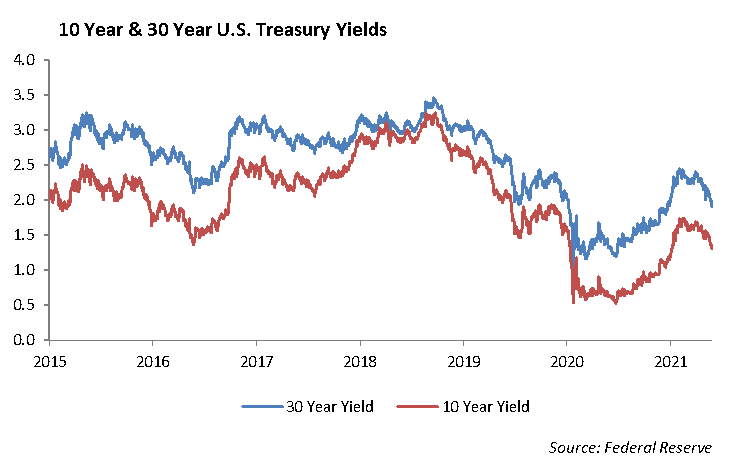

The bond market continues to reflect a strong belief that above-average inflation will be short-lived, and that the Fed’s ability to reduce quantitative easing will be limited. The rate on the 10-year U.S. Treasury continued its decline by over -10 bps last week. The interest rate on the 30-year U.S. Treasury dipped firmly below 2%, hitting a low of 1.88%. Much of this decline is being driving by the fact that banks are sitting on record amounts of cash, while at the same time, growth in the M2 money supply is decelerating significantly, and the velocity of M2 continues its sharp decline. We see the only catalysts for rates to move higher as a hard pivot from the Fed to end and unwind quantitative easing sooner and more aggressively than the market expects. We find it difficult to imagine a scenario where Jerome Powell would make this policy shift heading into the end of his current term as the head of the Federal Reserve. A more likely scenario is that the Fed will remain slow to pivot to keep capital markets stable.

Despite declining rates and increased volatility in equity markets, credit spreads have remained firm. This has been supported by light primary issuance due to the Fourth of July holiday, yet there is still strong demand for anything that pays a yield above inflation rates. We expect credit spreads to remain tight over the near term as volatility should generally remain suppressed. In low-volatility environments, investors should expect spread product to outperform risk-free assets regardless of directional moves in interest rates. We currently prefer an “up in quality” strategy, which gives our portfolios downside protection and dry powder to move out the risk curve when we experience a meaningful market correction.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management