By most measures, the period following the pandemic has been challenging for investors. Central banks of developed countries, led by our own Federal Reserve, completely missed the acceleration in the rate of inflation in the system. The Federal Reserve’s response to the unseen inflation was to push interest rates higher at a pace investors had never experienced. At the same time, corporate earnings stumbled and expectations for a slowing economy and increased unemployment became part of the narrative.

Yet, in spite of growing economic uncertainty, the S&P 500 index produced a solid total return of 26.29% for 2023. With this backdrop of economic uncertainty and optimism over the declining rate of inflation, we offer up the following investment themes for 2024.

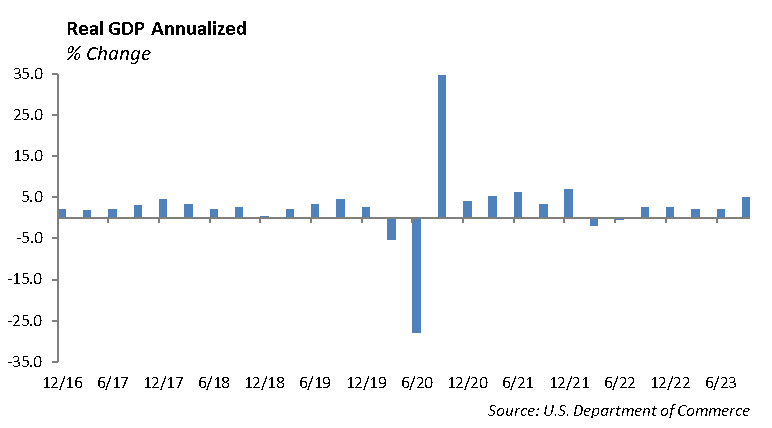

Economic Growth Should Slow as Consumer Spending Slows

We were surprised by the strength and resiliency in domestic economic growth this past year in the face of an aggressive tightening in monetary policy. However, we expect economic growth to be more subdued and the rate of inflation to decline in 2024. According to the U.S. Department of Commerce, real gross domestic product (GDP) increased at an annual rate of 4.9% in the third quarter of 2023, but we anticipate growth to fall below 3% for 2024. The U.S. consumer was the engine for domestic economic growth in 2023. Consumption should moderate in 2024.

Uncertainty in Fed Monetary Policy will be a Key Driver for the Level of Interest Rates

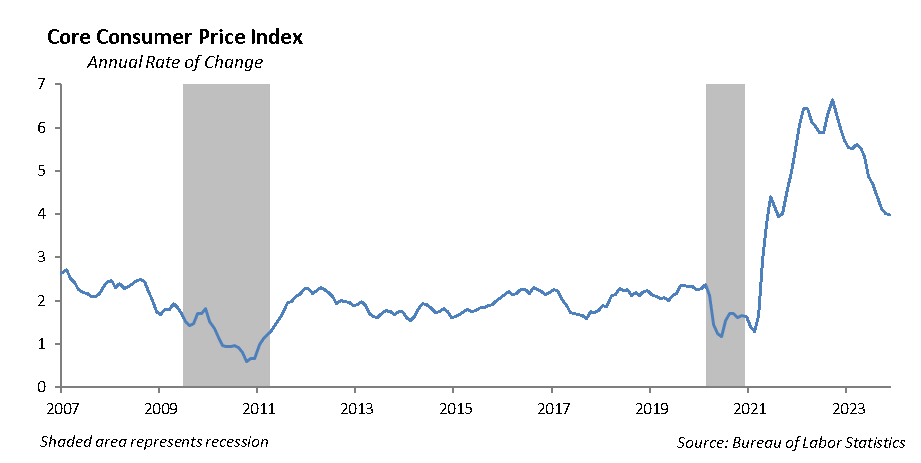

The rate of inflation continues to decline, real wage growth is slowing, and consumer spending is slowing. This combination of slowing economic data and the decelerating rate of inflation will lead the Fed to eventually lower interest rates in 2024. The surge in the rate of inflation peaked in June 2021 at 9.1% measured by Consumer Price Index (CPI) and has settled down to a 3.2% annual pace based on October 2023 data. It will be difficult for consumer spending to accelerate without significant growth in wages, which has been moderating at 3.4%.

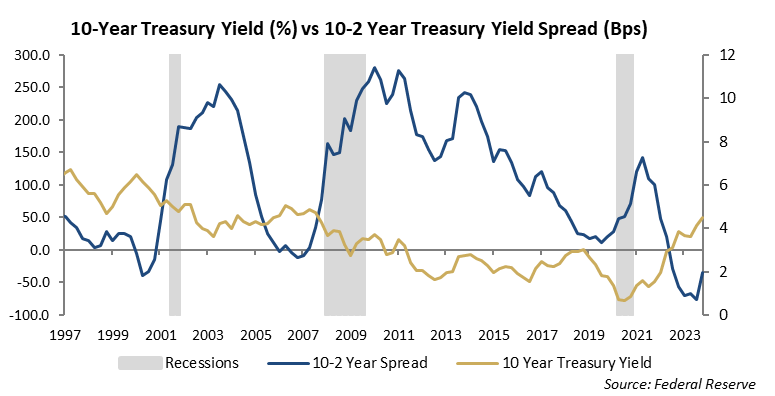

The Federal Reserve’s initiative to increase short term interest rates by 525 bps over the past 18 months forced the yield curve to invert so that yields on short US Treasuries are higher than longer dated US Treasuries. The move higher in interest rates over the past year has made investments in fixed income assets more appealing for 2024.

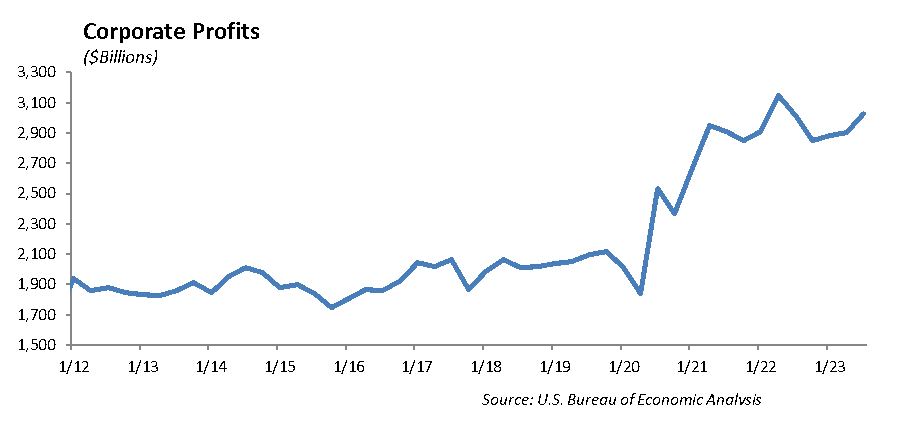

Corporate Profits Should Improve in 2024

After a year of dismal growth in corporate earnings, we expect to see improved growth next year. Corporate expense austerity programs, which includes lay-offs and expense reduction, increased last year to preserve profit margins. We project S&P earnings to grow 11% in 2024 to reach $240. Every S&P sector is expected to report positive EPS growth, with the strongest growth numbers coming from healthcare and info tech. These sectors will likely grow earnings over 25% in 2024. Earnings per share of $240 for the index puts the forward valuation at roughly 19x earnings. The 5-year median P/E ratio for the index is 19x. Using this estimate, fair value for the S&P 500 is about 4,700. Last year’s market gains occurred despite no growth in earnings. Strong earnings growth in 2024 will play a pivotal role as a catalyst to keep the market at current valuations.

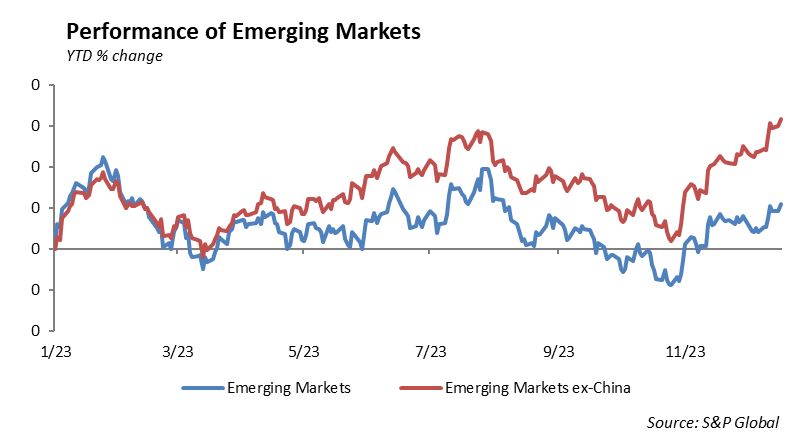

US Equities Should Outperform Developed Countries; However, China Appears to be Undervalued

Chinese equities fell significantly in 2023, recording a 15% drop over the last year and a 28% drop over the last 5 years. Meanwhile, domestic equities rose 80% over the last 5 years and international equities rose 20%. China has fallen out of favor with investors given its harsh regulatory standards, delisting risks, and geopolitical tensions, making investment in China difficult. However, Chinese equity valuations are among the cheapest with a forward price/earnings ratio of 12x. The China index has a 5-year average of 15x with highs of 21x. The S&P 500 is trading over 20x earnings and the IEFA is trading close to 16x. Over the last year, China softened its stance on regulations for big tech companies and provided audit data to U.S regulators, eliminating delisting risk. China has had geopolitical issues for decades, and the pullback of Chinese equities now provides a significant opportunity in the market.

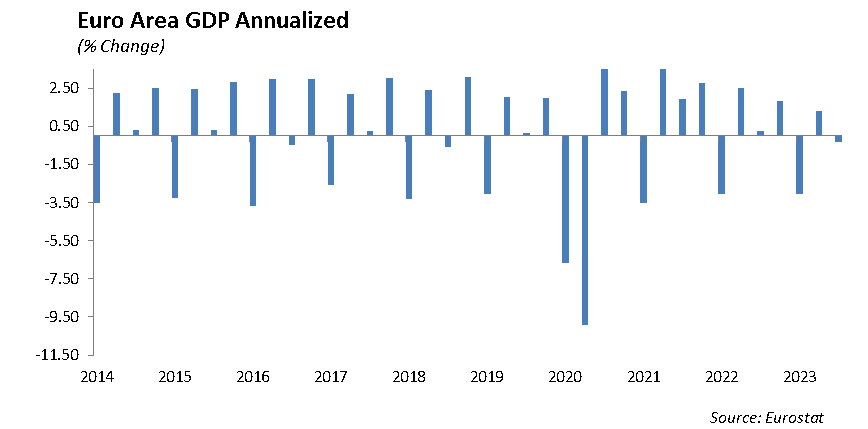

Economic Growth in Europe Will Improve in 2024

We expect growth in the European region to improve slightly to 1.6% but remain subdued for much of 2024. Conflicts in Europe and the Middle East will put pressure on aggregate demand as resources shift to support the conflicts. Employment should remain relatively stable and inflation should trend lower through the year. The economic engine for Europe is Germany, where inflation has been running over 3.5%. The improved economic outlook and lower inflation will help support lower cost of capital and positive outlook for European stocks. While the war in Ukraine will weigh on the European economy in 2024, we believe there is a growing opportunity in European equities given current valuations.

Large Cap Technology Stocks May Underperform the Broad Market

The strength in the equity market measured by the S&P 500 in 2023 is deceiving. Given the large concentration in the S&P 500 index of the top seven stocks by market capitalization, much of the outperformance can be attributed to the performance of these “mega cap” firms. The rebound has not been broad-based. The technology sector accounts for almost 30% of the index and increased by 55% in 2023. Furthermore, the five largest companies (Apple, Microsoft, Alphabet, Amazon, Nvidia) make up nearly 25% of the market capitalization of the S&P 500. The concentration of technology within the S&P is also understated given sector classifications. Stocks in the communication services sector, such as Alphabet and Meta, along with stocks like Amazon and Tesla which fall into the consumer discretionary sector, are all essentially technology companies. The weight of technology in the index approaches 40% if these factors are considered. Given premium valuations for mega caps, we expect outperformance of smaller cap stocks and would lean towards owning equal weight ETFs to capture that outperformance in 2024. This strategy takes an overweight position in smaller market cap firms compared to the S&P 500, while simultaneously reducing the exposure to large tech firms.

Stocks in the Banking, Healthcare and Cybersecurity Sectors Should Perform well this Coming Year

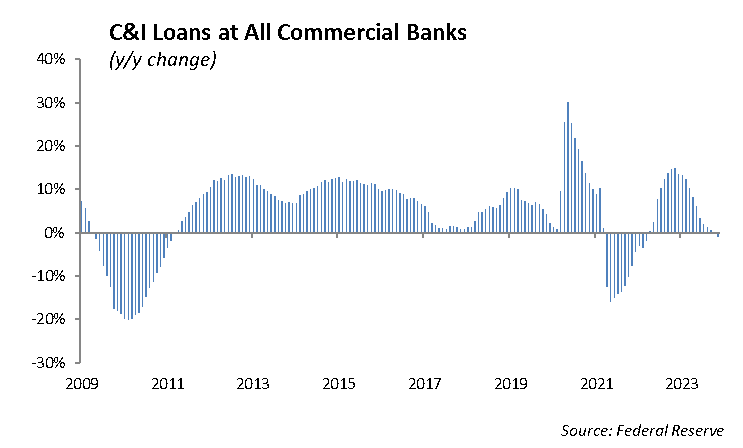

Banks faced extreme stress in 2023 with rising rates affecting their profitability, liquidity, and capital. Banks were forced to raise deposit rates in lockstep with the Federal Funds rate to avoid depositor disintermediation to money market mutual funds, increasing deposit costs, and tightening net interest margin. Further, the rapid rise in rates generated unrealized losses in the bank’s unhedged, long-dated bond portfolios, inhibiting on-balance sheet liquidity and damaging capital ratios through other comprehensive income. As we likely approach an easing Federal Reserve regime, we will see banks perform well through 2024. Lower rates provide relief on the sector’s deposit costs as well as unlock potential on-balance sheet liquidity by way of rising bond prices. Just as the banking sector suffered from rapidly raising rates in 2023, so too will it benefit as rates likely continue their downward trend in 2024.

We expect the healthcare sector could rebound after a drop in 2023, with a newfound interest in weight loss drugs and the return of M&A. In 2023, the sector fell 6% to under 19x earnings. In 2022, healthcare M&A fell 40%. The trend continued in the first half of 2023 as companies remained patient due to market uncertainty. The return of acquisitions is likely as inflation and interest rates stabilize, giving acquirers more flexibility. Additionally, biotech valuations have fallen 30% over the last 3 years. Large pharmaceutical companies need innovative solutions from biotech and these discounted companies will increase the demand for bolt on acquisitions to scale up and gain access to new markets and products. Finally, innovation is another reason for momentum within this sector, which we have seen with the GLP-1 market. Companies will position themselves to participate in the growth opportunity provided by weight loss drugs, presenting investors with many catalysts.

The growing threat of cyberwarfare has forced companies and governments to invest heavily in cybersecurity. Double-digit growth is expected for the foreseeable future with cloud security, data security, and identity access management being the main segments. As data becomes more accessible from cloud, laptops, personal computers, smartphones, and social media, criminals have more areas from which to attack. We have a seen many high-profile hacks over the last few years including Visa, Target, Home Depot, JP Morgan, and Equifax. The global cybersecurity market size was valued at $185 billion in 2021 and is expected to expand at a compound annual growth rate of 12% for the next 8 years. Cybersecurity is one of the most important industries in the coming decade and with the continued digitization, requirement for greater security will continue to increase.

Commercial Real Estate Recovery Gains Traction

Commercial real estate is a significant cog in the gears of the capital markets and an important asset class for investors. Since the pandemic, sectors within the commercial real estate market have been through turmoil as a result of supply chain disruptions and the trend in working from home. As a result, there has been significant stress in the operating fundamentals of the real estate market as well as pressure on valuations. 2024 will see improvement in the sector as loan modifications are settled, cost of capital declines, and capital availability improves. The oversupply of multi-family properties will slow absorption rates. The fundamentals in the office sector should improve as more workers return to the office and inventory of unleased office space is leased. We favor investments in the industrial warehouse, data storage, self-storage, and multi-family property types, and we are cautious on office and senior-living properties.

Structural Shifts in the Capital Markets Help Credit Expansion

The growth in private and structured credit continues to support major structural shifts in the capital markets that have taken place over the past decade. Loan underwriting by non-bank middle market lenders and bank loan syndication has diluted the banking sector’s role as the major source for credit expansion. This has resulted in a transfer of risk from banks into the capital markets in the form of collateralized loan obligations (CLOs) and other structured securities. The result is that the underlying credit risk of the collateral is pushed from that bank’s loan portfolio and into pension funds, endowments, insurance companies, and other portfolio entities that invest in private credit and structured credit instruments.

On one hand, this has created outstanding investment opportunities for institutional investors able to access these private investments. On the other hand, the growing risks to the capital markets are unknown given the lower level of regulatory oversight in the private credit market. While CLO’s performed well during the financial crisis in 2009, the plumbing in the capital markets may not be sufficient to support the growth in the sector. This could create systemic risk given the pervasive distribution of private and structured credit through the capital markets.

Lower Expected Returns for Risk Assets

With the year-end rally, the S&P 500 posted a total return of 26.2% for 2023. Equity valuations are again stretched to high levels. This is an impressive rate of return considering that, during much of that time, parts of the economy were effectively shut down due to the pandemic, the U.S. trade policy with China was in a shambles, and war between Russia and Ukraine disrupted global economic growth. Over the four-year period of 2019-2022, domestic equities returned an average annualized rate of 17.4%. For much of the past year, investors were forced to navigate the banking crisis, persistent inflation, the Fed’s tightening monetary policy, and a slowing economy into their valuation models.

The S&P 500 is currently trading at over 24.3x earnings, well above the long-term market average of 16.5x and the 19x average over the last 5 years. While we expect reasonable earnings growth in 2024, these heightened valuations will still be a headwind for stocks in 2024. We believe this will lead to lower expected returns over the next few years until it is clear that the Federal Reserve has declared victory on inflation and normalizes monetary policy.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2024 Winthrop Capital Management