The Economy

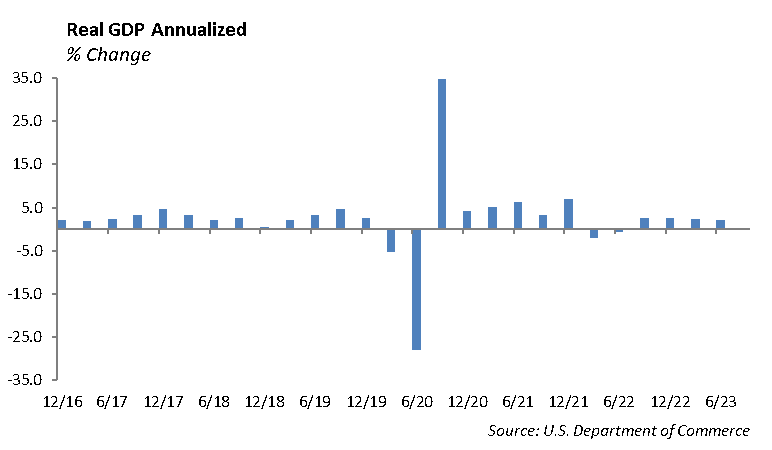

The U.S. economy has been resilient this year. Measured by its output, the gross domestic product (GDP) increased 2.6% in 3Q 2023, greater than the 2.0% increase in 1Q 2023.

This growth rate is impressive considering the increase in interest rates over the past year. The Federal Reserve continues to maintain a restrictive monetary policy in an effort to shift aggregate demand lower and reduce the rate of inflation.

While the Fed continues a restrictive monetary policy, the federal government continues to maintain a budget deficit of more than $1 trillion. As a result, a stimulative fiscal policy is working to counteract the effects of restrictive monetary policy.

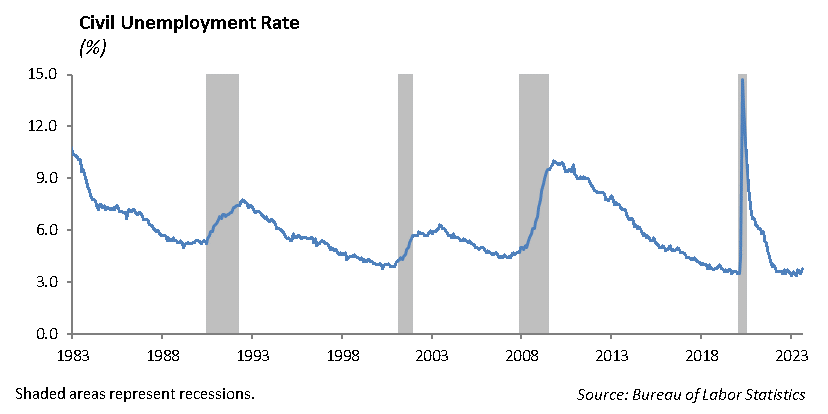

The labor market remains strong. Employers added 1.6 million jobs through 3Q 2023, and the unemployment rate is running at 3.8% in September as reported by the Bureau of Labor Statistics. The labor force participation rate increased from 60.1% in April 2020 to 62.8% in September 2023.

For the second half of 2023, we expect deterioration in the health of the consumer sector. An increase in corporate layoffs is beginning to erode the strength in employment. The consumer savings rate has slipped to 3.9%, while domestic household and credit card debt reported by the Federal Reserve has increased to over $1 trillion. At the same time, the requirement to pay interest on student loan debt was reinstated on October 1st. Similarly, higher interest rates on auto loans and home mortgages are acting to slow economic growth.

Employment data, including the non-farm payrolls and the ADP jobs report, have supported the robust economic growth, and have exceeded market expectations. This sustained strength in the labor market, in the face of rising short-term interest rates, suggests the need for additional monetary tightening.

The current level of employment growth matches trend line growth and illustrates the economy shedding the long-term effects of the pandemic. However, the size of the labor pool, measured by the labor force participation rate, has been slower to recover as workers opted for retirement or simply left their jobs.

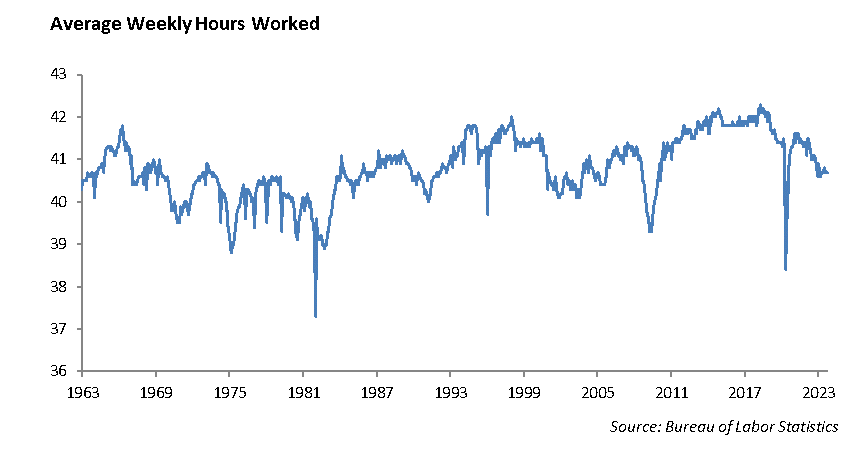

The seasonally adjusted average hours worked per week was 34.4 hours in September, significantly lower than the 35-hour peak measured in January 2021. There also remains a shortage of labor in certain industries.

As a result, the notion that the Fed has “more work to do” is slightly flawed and we expect the recent increase in treasury yields to reverse its course in the first half of 2024.

Monetary Policy

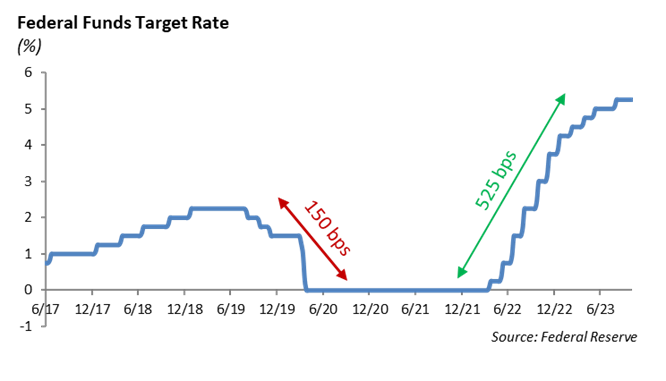

The key driver to the Federal Reserve’s monetary policy this year will be the direction and pace of inflation. The Fed has tightened monetary conditions over the past two years by increasing the Fed Funds rate 525 basis points in an effort to shift aggregate demand lower. However, stimulative fiscal policy, expressed through large deficit spending, has helped support continued strong economic data.

After a historic increase in short-term interest rates over the past two years, the Fed paused its tightening program in May. It takes time for the higher interest rates to work through the economy and we expect the Fed to take a “wait-and-see” approach to determine if further tightening is warranted.

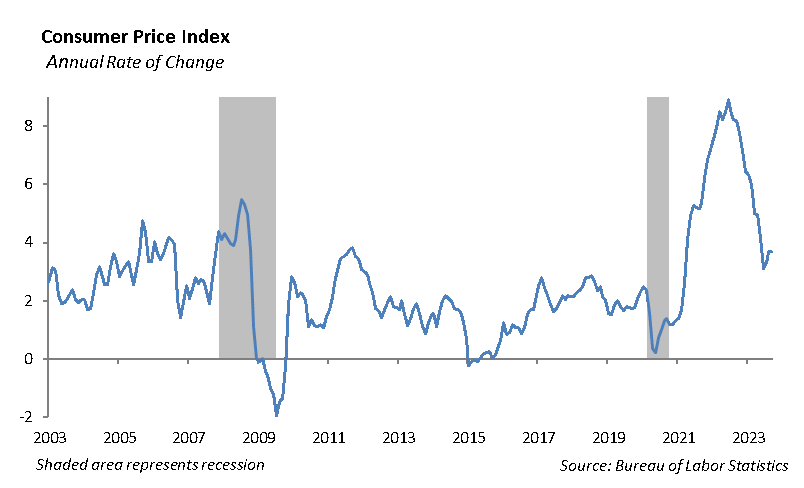

The inflation rate, as measured by the CPI, has fallen from its levels in 2022 to 3.7% for September. While we expect inflation to continue to decline, it will take more time and further tightening to reach the 2% inflation target established by the Fed.

We expect the Federal Reserve will likely need to increase the Fed Funds rate again in 4Q 2023 given the positive economic data. Fiscal deficits, typically near 3%, have been running over 10% the past four years. We believe this is unsustainable to maintain stability in the economy and capital markets. Until domestic fiscal spending is under control, we expect to stay above 3%.

Valuations Shift in Equity Market

The S&P 500 declined -3.3% during the third quarter of 2023. Rising global interest rates, concerns over a rebound in inflation, and the potential for an economic slowdown weighed on the domestic equity market. In addition, with growing concerns in the housing market and mortgage rates hitting 7.5%, consumer confidence hit a 4-month low. Student loan payments restarting in October added additional pressure on the consumer.

During the quarter, the Energy sector was by far the best-performing sector which benefited from higher oil prices. The communication services sector finished second, increasing by 2.8% led by Alphabet (GOOG/L) and Meta (META). Real estate and utilities, on the other hand, trailed with quarterly decreases of -9.7% and -10.1%, respectively. Both sectors were negatively impacted by higher interest rates.

On a year-to-date basis, communication services (+39.4%), technology (+33.8%), and consumer discretionary (+25.7%) are the best performing sectors within the S&P 500. The U.S. market, measured by the S&P 500, performed better than the MSCI EAFE index by a slight margin, with support from the strength of the US dollar. In emerging markets, all three market regions showed minor decreases this quarter. EMEA dropped -1.8%, Emerging Asia declined -2.2%, and Latin America lost -2.7%. We believe the AI frenzy has led to extended valuations in the market, as the Nasdaq has risen 27.1% year-to-date. Tech stocks, including Microsoft, Tesla, Meta, and Alphabet, have benefited from an AI premium this year.

We expect the performance of the defensive sectors, which include health care, utilities, and consumer staples, to perform better than the broad market given current valuations. Historically, these sectors outperform in recessionary environments. The growth sectors are still trading more expensive relative to the index, with valuation of technology stocks averaging 31x earnings and consumer discretionary stocks at 29x earnings.

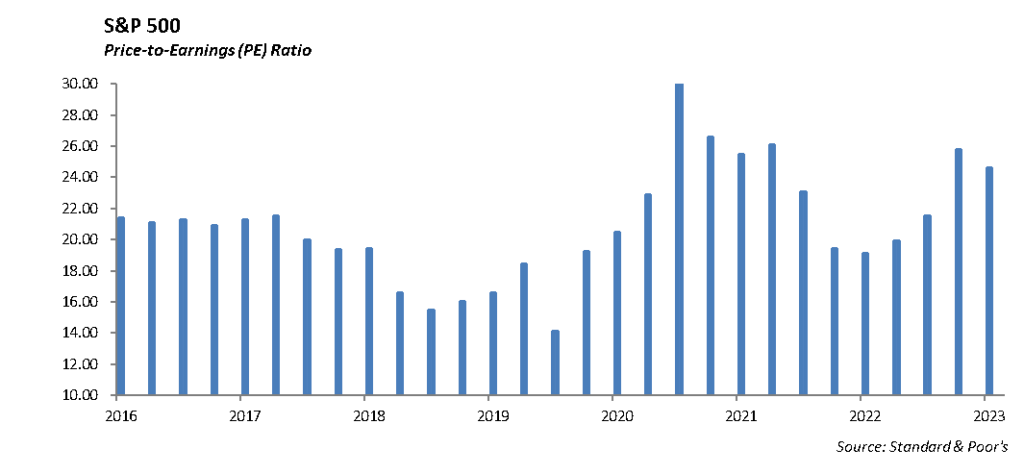

As of the end of the third quarter, the S&P was at the 4288 level and trading at 21x earnings. We believe the market remains overvalued, providing minimal upside from current levels and a tough fourth quarter ahead.

Opportunities in Fixed Income

As long as the rate of inflation is declining, we expect interest rates to stabilize, and the bond market becoming less reactive to the Fed’s next anticipated move. With a stable monetary policy, we would expect lower volatility to create investment opportunities across the fixed income markets, given the elevated level of interest rates across the curve.

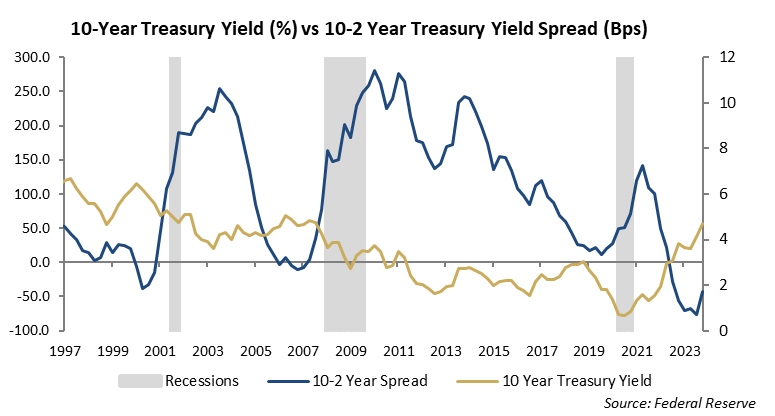

Investors have not experienced this level of the inversion in the yield curve, as well as the length of time the curve has remained inverted, in over 30 years. We expect the yield curve to remain inverted through the second half of the year until slowing economic growth and a lower rate of inflation provides cover for the Fed to lower short-term rates.

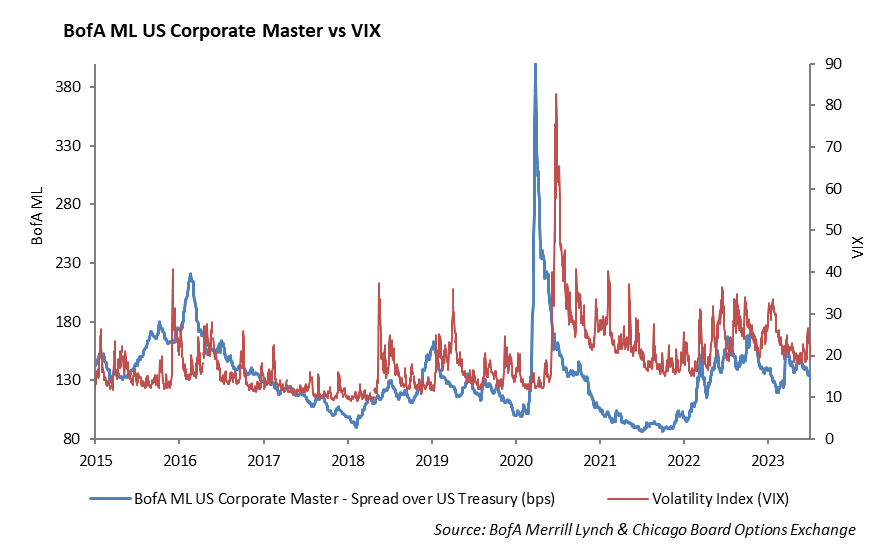

Currently, 5-year BBB rated corporate bonds are yielding above 6.00% and similar maturity high yield BB rated corporate bonds are yielding over 6.50%. With the yield on the 10-year US Treasury at its highest level since October 2007 and credit spreads trading at their widest levels in the past five years, we are seeing more buying opportunities in the fixed income market.

Structured securities remain one of the cheapest sectors in the fixed income market. The CLO market has experienced spread widening this past year; however, credit quality has remained strong. At the same time, underlying deterioration in the collateral supporting CMBS has forced spreads wider over the past year. Refinancing and credit risk in commercial real estate is causing pain in both loans and securitized markets.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2023 Winthrop Capital Management