A year ago, we discussed on this podcast the spread of COVID-19 and how it was affecting the capital markets. March 16, 2020 was the worst one day sell-off in stock prices since 1987. The S&P was down -26% year-to-date, and bond yields declined to historic low levels. At the same time, volatility spiked to four times the normal rate.

Let’s go through our initial expectations for the economy after the dramatic downturn, and compare to the results that have unfolded throughout the past year.

Global Economic Growth

On March 16, 2020, we expected global growth to be negatively impacted by the coronavirus.

The Result – Global growth took a dip in 2020, declining -3.4%, according to the Organization for Economic Cooperation and Development (OECD). Now, it’s expected to increase by 5.6% this year, though it will be lopsided, based on each country’s ability to control the virus and resume output.

Our Take – Near-term economic growth will be dictated by the intersection of fiscal stimulus and mass distribution of the COVID-19 vaccine. On its own, either factor is unlikely to spark meaningful growth to push the economy above its pre-pandemic levels in the near term. The pandemic led to more than 22 million jobs lost, and while circumstances are improving, the U.S. workforce has only recovered 60% of those lost jobs. We believe the U.S. economy will grow by 6% in 2021 as vaccinations are quickly distributed and a third stimulus package cultivates a resurgence of consumer spending equivalent to the Roaring Twenties. In the past, the U.S. Economy has pushed the global economy forward, and we believe this time around will be no different. With that said, we still believe structural and demographic issues will limit the growth in both Europe and Asia.

Company Earnings

We expected that certain industries, including the energy pipeline, mall REITs, and food service, would be challenged during this period.

The Result – Earnings season has unofficially ended, and although expectations have been quite low all year, the historical comparisons are staggering. Last year, we saw three of the strongest earnings and revenue beat rates in history, with an average of more than 75% of companies beating expectations. Additionally, guidance raises have been fairly strong.

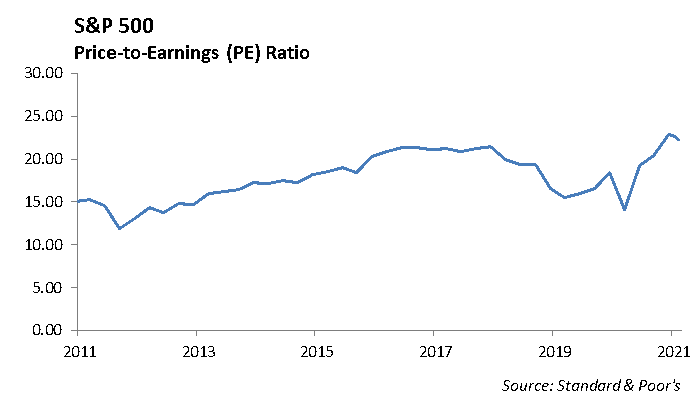

Our Take – Economic growth will drive company earnings as consumers are more willing and able to spend. We expect 2021 earnings for the S&P 500 to come in $165 per share, a 33% increase over 2020. Despite this growth expectation, the forward price-to-earnings ratio will remain above 22. This is much higher than the historical 15x historical ratio.

Residential Housing

We expected the residential housing market to slow over the near term as consumers shift priorities toward increasing savings.

The Result – Residential sales have been strong, despite the pandemic, job losses, and low inventory. Housing prices have climbed, and cash-out refinancing climbed 42% last year, according to the National Association of Realtors.

Our Take – Residential housing will likely begin to flatten out as the initial surge in moving out of cities has begun to slow. Further, the 12-month forbearance period for many people will begin to come due in April. We estimate 30% of residential mortgages are in forbearance. Once this period runs out, we may see a spike in homes for sale due to the inability to afford the payments. Overall, low inventory and accelerating input costs for new homes will support home values even if we see more homes hit the market.

Interest Rates

We expected the Federal Reserve would maintain low interest rates to keep the economy moving and provide liquidity in the market.

The Result – Federal Reserve Chairman Jerome Powell has said he intends to keep interest rates low until the labor market is stronger, inflation hits its 2% target and is expected to remain at that level or higher.

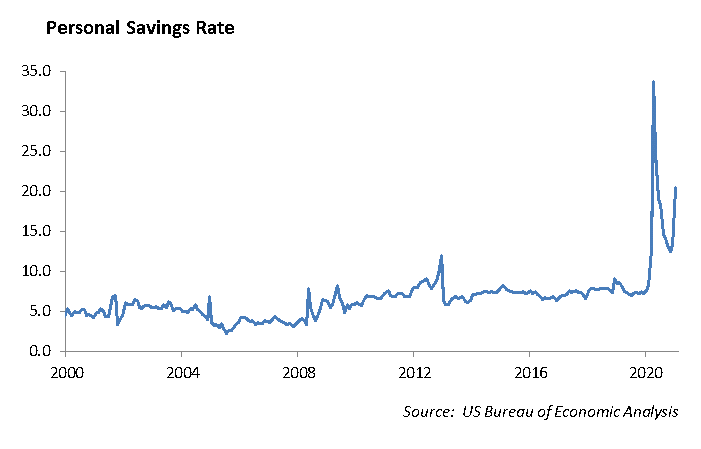

Our Take – The future path of interest rates will be directly correlated with the rate of economic growth and inflation. While economic growth is very likely, inflation is more difficult to predict. Both monetary and fiscal policies have been loose over the past year, but it has not lead to accelerating inflation. Increased savings rates and bank reserves has led to less money flowing through the system, muting inflation. The acceleration in economic growth will likely lead to a short-term increase in interest rates; however, we believe interest rates will likely remain in a decline over the long run. An aging population of savers and accelerating technology are some of the key factors pushing down both inflation, and hence, interest rates.

Airline Industry

We expected the airline industry would require a bailout, much like the TARP program offered to banks during the 2008 Financial Crisis.

The Result – Bailouts have come in waves for the airline industry, as three surges: in April, as $25 billion in grants and loans to pay flight attendants, pilots and other employees; in December, $15 billion for payroll assistance; and last week, additional payroll funding to the tune of $14 billion.

Our Take – Regardless of any stimulus, bailouts, vaccines, or economic growth, it is extremely unlikely that the airline industry returns to its pre-pandemic revenue any time soon. The virus changed consumer behavior, and in many ways showed us that there is a better way to do things. Business travel is going to be the biggest negative shift for airlines. The adoption, acceptance, and preference of a virtual business meeting means that airlines will not be able to count on the business travel who would once pay any price for a last-second ticket. Of the domestic airlines, Southwest is best positioned due to their low debt, domestic-based travel, and focus on vacation travel over business travel.

Price of Financial Assets

We expected prices of financial assets would normalize as more information was discovered about the virus.

The Result – This area has been more of a wild card, as the Dow and S&P 500 have hit record highs recently. Bond prices are at risk with rising inflation, and the Federal Reserve may have more to say about that as they meet this week.

Our Take – Valuations across all risk assets are historically stretched. With rates still at historically low levels and credit spreads near all-time tights, it is difficult to find a safe-haven asset. Commodities have even accelerated as supply-chain issues have driven up the prices of construction inputs. We believe this will compress returns over the next 3-5 years, as the investors have pushed the returns of many years into one or two. We still believe the economic growth picture will lead to positive asset returns, but we are managing investor expectations of what future returns will look like.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management